As first time buyers in today’s Canadian real estate market, you might be facing unique challenges: rising interest rates, competitive bidding wars, and the stress of making such a major investment. Let’s get right into it!

Bonus Tool: Try our BMI Mortgage Penalty Calculator to see exactly what breaking your mortgage could cost—most buyers don’t realize these fees until it’s too late!

Detailed Glossary of Mortgage and Real Estate Terms

To navigate the complex world of Canadian mortgages, a solid understanding of key terminology is essential. Here’s a comprehensive glossary to help you decode the jargon:

- Amortization: The gradual repayment of a loan over a specified period.

- Appraisal: An expert’s estimate of the value of a property.

- Blended Mortgage: A mortgage that combines fixed and variable interest rates.

- CMHC Insurance: Mandatory mortgage default insurance for high-ratio mortgages.

- Conventional Mortgage: A mortgage with a down payment of at least 20%.

- Debt-to-Income Ratio (DTI): The percentage of your gross monthly income that goes toward paying debt.

- Equity: The difference between the current market value of your home and the amount you still owe on your mortgage.

- Fixed-Rate Mortgage: A mortgage with an interest rate that remains the same throughout the term.

- High-Ratio Mortgage: A mortgage with a down payment of less than 20%.

- LTV (Loan to Value): The ratio of your mortgage loan amount to the appraised value of the property.

- Mortgage Broker: An intermediary who connects borrowers with lenders.

- Open Mortgage: A mortgage that allows for prepayment without penalties.

- Pre-Approval: A lender’s preliminary assessment of how much you can borrow.

- Prime Rate: The interest rate that commercial banks charge their most creditworthy customers.

- Reverse Mortgage: A mortgage that allows homeowners aged 55 and older to access their home equity.

- Variable-Rate Mortgage: A mortgage with an interest rate that fluctuates with the prime rate.

And many more terms related to provincial laws, and specific financial instruments.

Case Studies: Mortgage Scenarios

Let’s examine some real-life mortgage scenarios to illustrate the practical application of the information discussed:

Case Study 1: The First Time Homebuyers in Toronto

Sarah, a young professional in Toronto, wants to buy her first condo. She has a limited down payment and is concerned about rising interest rates. We’ll analyze her options, including high-ratio mortgages, government assistance programs, and strategies for managing variable-rate risk. We will also discuss the effects of condo fees on her purchasing power.

Case Study 2: The Family Upgrading in Vancouver

The Patel family is upgrading to a larger home in Vancouver’s competitive market. They need to navigate high property values and explore options for bridging loans and portable mortgages. We’ll discuss their strategies for maximizing equity and minimizing closing costs.

Case study 3: The Rural Property in Alberta

John and Mary are looking to buy a farm property in rural Alberta. They need to understand the unique challenges associated with rural properties, and the types of lenders that will provide mortgages on these types of properties. We will also look at the risks associated with these types of properties.

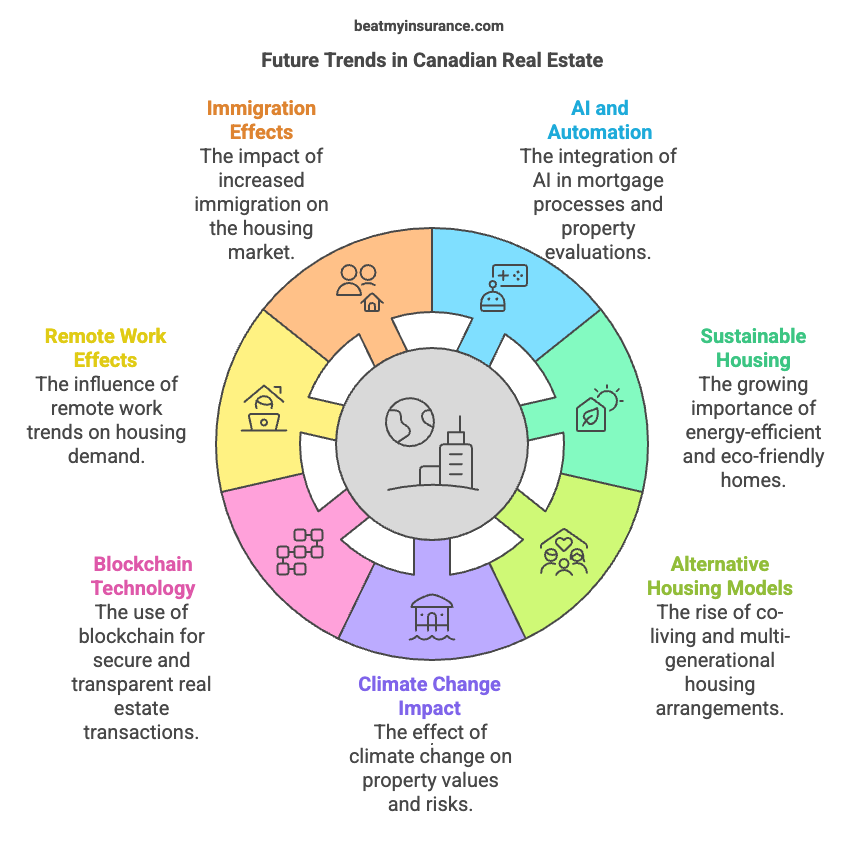

Future Trends in Canadian Real Estate and Mortgages

The Canadian real estate and mortgage landscape is constantly evolving. Here are some future trends to watch:

- Increased Use of AI and Automation: AI-powered mortgage applications, property valuations, and risk assessments will become more prevalent.

- Growing Demand for Sustainable Housing: Energy-efficient homes and green building practices will become increasingly important.

- Rise of Co-Living and Multi-Generational Housing: Changing demographics and affordability challenges will drive demand for alternative housing models.

- Impact of Climate Change on Property Values: Coastal properties and regions prone to extreme weather events will face increased risks.

- Blockchain Technology in Real Estate: Blockchain could revolutionize real estate transactions, making them more secure and transparent.

- The effects of work from home, on the housing market.

- The effects of increased immigration on the housing market.

Provincial Assistance Programs

Each province offers unique assistance programs for homebuyers, particularly first time buyers. Below is a detailed overview of these programs across Canada.

Ontario

Land Transfer Tax Refund

First time homebuyers in Ontario can receive a refund of land transfer tax up to $4,000. This effectively eliminates the land transfer tax on homes purchased for up to $368,333.

First Time Home Buyers’ Incentive

The provincial government works with the federal program to offer 5-10% of the home’s purchase price to put toward a down payment, reducing monthly mortgage payments.

British Columbia

First Time Home Buyers’ Program

This program offers a full or partial exemption from the property transfer tax for eligible first time homebuyers purchasing homes valued up to $500,000.

BC Home Owner Mortgage and Equity Partnership

This initiative helps first time homebuyers by matching a portion of their down payment with an interest-free loan for the first five years.

Alberta

Alberta Mortgage and Rent Assistance Program

This program offers financial assistance to Albertans with low income to help them afford their housing costs. It provides support for both renters and homeowners with mortgage payments.

Quebec

AccèsFamille Program

This Quebec-specific program assists families with children to purchase their first home by providing financial aid and favorable loan terms based on family size and income.

Other Provincial Programs

Manitoba

The Rural Homeownership Program assists low-to-moderate income households in rural Manitoba to become homeowners through down payment assistance.

Nova Scotia

The Down Payment Assistance Program offers interest-free loans to first time homebuyers to help with their down payment.

Saskatchewan

The HeadStart on a Home program supports the construction of entry-level housing with potentially lower down payment requirements.

Canadian Mortgage Market for New Immigrants

Challenges & Solutions:

- No Canadian credit history? Learn how to build it fast (spoiler: secured credit cards help!).

- Language barriers? Many lenders offer multilingual support—we’ll point you to them.

Investing in Canadian Real Estate

Rental Properties

- Location hacks: Why “near transit” beats “trendy neighborhood” for steady income.

- Landlord 101: Screen tenants like a pro (free template included!).

- Tax wins: How depreciation can lower your taxable income.

REITs (No Landlord Headaches!)

- What they are: Like stocks, but for apartments/malls you don’t have to manage.

- Best for: Busy folks who want real estate exposure without midnight plumbing calls.

Flipping Houses

- The ugly truth: 1 in 3 flippers lose money. Here’s how to be the 2 who profit.

- Must-have team: Why your contractor matters more than your selling price.

Airbnb & Short-Term Rentals

- Hotspots: Where tourists pay top dollar (and where bylaws will fine you).

- Tax trap: The CRA always notices rental income. Report it right.

Green Homes = Smarter Homes

- Energy-efficient mortgages: Get lower rates for solar panels/insulation.

- Gov’t cash: Rebates for heat pumps, windows, and more (up to $5,000 back!).

- Future-proofing: Wildfire-resistant siding? Flood-proof basements? Yes, it’s a thing.

Home Inspections & Insurance

Inspections

- Red flags inspectors miss: Knob-and-tube wiring, polybutylene pipes.

- Land surveys: Why your dream yard might legally belong to the neighbor.

Insurance

- Climate change impact: Why your premium doubled (and how to fight back).

- Claims made easy: Photo everything before moving in (seriously).

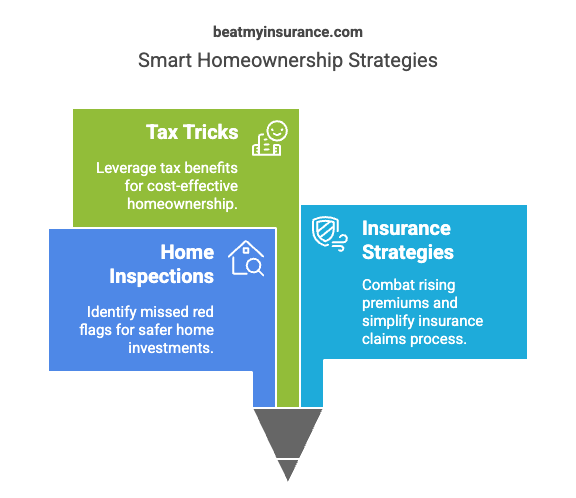

Tax Tricks for Homeowners

- Capital gains: Live in your rental for 1 year = pay $0 tax when selling (*conditions apply).

- Home office hack: $500/year deduction without receipts.

Provincial Power Guide (2025 Trends)

| Province | Hot Trend | Watch Out For |

|---|---|---|

| Ontario | Co-living spaces (affordable urban hack) | Bidding wars in GTA suburbs |

| BC | Floating foundations (sea-level rise) | Strata insurance spikes |

| Alberta | “Agrihoods” (farm + community living) | Oil market volatility |

| Maritimes | Tiny homes ($50k cabins) | Hurricane insurance clauses |

Home Inspections

A home inspection is your last line of defense before committing to a property. While most inspectors check the basics, some critical issues slip through the cracks. Here’s what to watch for:

1. Knob-and-Tube Wiring (Pre-1960s Homes)

- The Risk: Outdated, ungrounded wiring that can overheat and cause fires.

- Insurance Impact: Many providers refuse coverage unless it’s fully replaced.

- Cost to Fix: 8,000–8,000–15,000 for a full rewire.

2. Asbestos Insulation (Common in Pre-1980s Homes)

- Where It Hides: Around pipes, attic insulation, and old vinyl flooring.

- Key Rule: If undisturbed, it’s generally safe—but never attempt DIY removal.

- Testing Cost: $300–500 for professional assessment.

3. Polybutylene Pipes (Installed in the 1980s–90s)

- Why It’s Dangerous: Prone to sudden leaks and bursts.

- Check For: Blue or gray flexible pipes in basements or crawl spaces.

- Insurance Note: Some providers exclude water damage from these pipes.

4. Sewer Line Problems

- Must-Ask Question: “Has the sewer line been scoped?”

- Why It Matters: Tree roots or cracks can lead to $10,000+ repairs.

- Smart Move: Request a video inspection before closing.

5. Quick Cover-Ups

- Red Flags: Fresh paint in odd places (could hide mold or leaks), mismatched flooring patches.

- Pro Tip: Hire an inspector who uses thermal imaging to detect hidden moisture or electrical issues.

Bottom Line: Never skip a home inspection, and always attend it in person. A few hundred dollars now could save you tens of thousands later.

Why Rates Are Rising and How to Save

Home insurance premiums are climbing across Canada, thanks to extreme weather and inflation. Here’s what’s driving costs up—and how to fight back.

Why Your Premiums Are Increasing

- Climate Change Impact:

- Wildfire Zones (BC, Alberta): Some premiums have doubled.

- Flood-Prone Areas (Atlantic Canada): New flood maps mean more homes are deemed high-risk.

- Construction Costs: Inflation has driven up rebuilding expenses by 20–30% in some regions.

How to Lower Your Insurance Costs

- Bundle Policies: Combining home and auto insurance can save 10–15%.

- Upgrade Your Roof: Metal or impact-resistant shingles may qualify for discounts.

- Increase Your Deductible: Raising it from 1,000to1,000to2,500 can cut premiums by 10–20%.

- Install Security Systems: Some insurers offer discounts for monitored alarms.

Protecting Yourself from Claims Denials

- Before Moving In: Take dated photos of:

- Electrical panels (serial numbers).

- Water heaters (manufacturer date).

- Major appliances (model numbers).

- Ask About “Claims Forgiveness”: Some insurers won’t raise rates after your first claim.

Pro Tip: Review your policy annually—coverage needs change as your home ages.

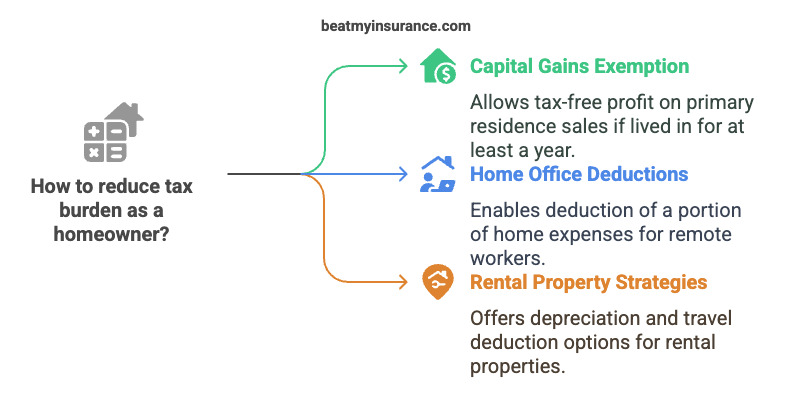

Tax Secrets Every Canadian Homeowner Should Know

The Canada Revenue Agency (CRA) offers several ways to reduce your tax burden as a homeowner. Here’s how to take advantage.

1. Capital Gains Exemption (Primary Residence Loophole)

- How It Works: If you live in a property for at least one year before selling, the profit is tax-free (up to $250,000 per owner).

- The “Plus One” Rule: You can claim the exemption for one extra year after moving out.

Example:

- Buy a condo in 2025 for $500,000, rent it until 2027.

- Move back in for 12 months (2027–2028), then sell for $800,000 in 2029.

- Tax Owed: $0 (if within limits).

2. Home Office Deductions (For Remote Workers)

- Deduct a percentage of mortgage interest, utilities, and maintenance.

- Example: If your office takes up 10% of your home, you can deduct 10% of eligible expenses.

Audit-Proof Tip: Keep a floor plan showing your workspace dimensions.

3. Rental Property Tax Strategies

- Depreciation (Capital Cost Allowance): Claim a portion of the building’s value each year (not the land).

- Travel Deductions: Track kilometers driven for property management (2025 rate: $0.68/km).

Warning: Always document expenses—the CRA may request proof.

Conclusion

As we come to the end of this thorough examination of the Canadian mortgage and real estate market, it is clear that a multifaceted strategy is necessary for successful homeownership in 2025 and beyond. The fundamentals of how Canadians buy and maintain their homes are changing due to the convergence of economic, technological, environmental, and social forces.

The real estate market in Canada is a patchwork of regional and even local subtleties. Every region offers a different set of opportunities and challenges, from the busy urban corridors of the GTA and Vancouver to the resource-rich terrain of Alberta and the tranquil coastal vistas of the Maritimes.

Strategic homebuying requires an understanding of these localized dynamics, not just an advantage. This calls for a thorough examination of market trends, infrastructure advancements, demographic changes, and provincial regulations. Once thought to be a simple transaction, the mortgage industry has developed into a complex web of financial products.

A sophisticated understanding of the interactions between open and closed mortgages, fixed and variable rates, and specialized products like reverse and blended mortgages is necessary.

Homebuyers must examine the nuances of amortization schedules, prepayment privileges, and the constant mortgage stress test in addition to the superficial comparisons.

Technology integration, like blockchain-based transactions and AI-powered mortgage applications, is set to further change this environment and necessitate digital literacy and flexibility.