A 35 Year Mortgage Canada amortization stretches the debt length and significantly increases the total interest paid over the lifetime; it also provides lower monthly payments and more near-term affordability.

Those who want to make wise decisions regarding whether a 35 year mortgage in Canada fits their long-term financial goals and general wealth creation must use strategic financial planning, and leverage tools like the “Beat My Insurance Mortgage Penalty Calculator” to understand the nuances of the Canadian mortgage market, critically evaluate the opportunity cost, and engage in ongoing financial education.

Advanced Financial Modeling and Scenario Planning

Advanced financial modeling is absolutely essential if one is to really understand the long-term consequences of a 35-year mortgage. This means producing thorough simulations and projections to evaluate several possibilities.

Cash Flow Modeling: Develop a comprehensive cash flow model that incorporates all income and expenses, including mortgage payments, taxes, and investments.

Sensitivity Analysis: To find out how changes in important factors—such as income, interest rates, and expenses—impact your financial results, do sensitivity analysis. This helps you create backup plans and spot possible weaknesses.

Monte Carlo Simulation: As mentioned, this is a powerful tool for quantifying risk. Expand its use to include inflation, job loss probabilities, and complex investment return models. It allows you to generate thousands of possible outcomes, giving a realistic range of potential financial futures.

Time Value of Money Analysis: Use time value of money calculations to compare the present value of future mortgage payments and investment returns.

The Intersection of Tax Planning and Mortgage Strategy

Tax planning is an often-overlooked aspect of mortgage strategy.

Home Buyers’ Plan (HBP): Understand how the HBP can impact your mortgage decisions, especially if you’re a first-time homebuyer.

Tax Deductibility of Mortgage Interest: Explore advanced strategies for converting non-deductible mortgage interest into tax-deductible interest, such as the Smith Manoeuvre. “Consult with a tax professional to ensure compliance with tax laws.” (“Travel Nursing Tax Tips: Navigating The Road To Compliance”)

Capital Gains Tax: Consider the potential impact of capital gains tax on the sale of your property, especially if you’re planning to sell before the end of your amortization period.

Property Tax Considerations: A 35 year mortgage Canada may seem affordable today, but rising property taxes over decades could strain your budget.

The Role of Insurance and Risk Management

Without proper insurance, a 35 year mortgage Canada could leave homeowners vulnerable to financial shocks during the lengthy repayment period.

Mortgage Default Insurance: Understand the costs and benefits of mortgage default insurance, especially if you’re making a down payment of less than 20%.

Life Insurance: Consider purchasing life insurance to protect your family in the event of your death, ensuring they can continue to make mortgage payments.

Disability Insurance: Protect yourself against income loss due to disability by purchasing disability insurance.

Home Insurance: Ensure you have adequate home insurance to cover potential losses due to fire, theft, or other disasters.

Critical Illness Insurance: Consider critical illness insurance, which can provide a lump-sum payment if diagnosed with a critical illness.

The Impact of Technological Disruption on the Mortgage Industry

Technological disruption is transforming the mortgage industry, creating new opportunities and challenges.

FinTech and Online Lenders: Explore the offerings of FinTech companies and online lenders, which may offer more competitive rates and flexible terms.

Blockchain and Smart Contracts: Understand the potential impact of blockchain technology and smart contracts on the mortgage process.

Artificial Intelligence (AI) and Machine Learning: Explore how AI and machine learning are being used to automate mortgage underwriting and risk assessment.

Digital Mortgage Platforms: Leverage digital mortgage platforms to compare mortgage options, apply for mortgages, and manage your mortgage online.

Psychology of Long-Term Financial Commitment

The psychological impact of a 35-year mortgage cannot be overstated.

Cognitive Dissonance: Understand how cognitive dissonance can influence your mortgage decisions, leading you to justify choices that may not be in your best interest.

Sunk Cost Fallacy: Avoid falling into the sunk cost misbelief, which can lead you to continue paying a mortgage even if it’s no longer financially viable.

Delayed Gratification vs. Immediate Gratification: Balance the desire for immediate gratification with the need for delayed gratification, especially when it comes to long-term financial planning.

The Endowment Effect: Be aware of the endowment effect, which can lead you to overvalue your home and make suboptimal mortgage decisions.

Building a Resilient Financial Portfolio

A 35-year mortgage requires a resilient financial portfolio that can withstand market fluctuations and unexpected events.

Diversification: Diversify your investment portfolio across different asset classes, such as stocks, bonds, real estate, and alternative investments.

Asset Allocation: Develop an asset allocation strategy that aligns with your risk tolerance and investment goals.

Regular Portfolio Reviews: Conduct regular portfolio reviews to ensure your investments are on track.

Rebalancing: Rebalance your portfolio periodically to maintain your desired asset allocation. (“Effective Strategies for Long-Term Investing – Uber Finance”)

Emergency Fund: Expand your emergency fund to cover a wider range of potential expenses, such as job loss, medical emergencies, and home repairs.

The Social and Economic Ripple Effects of Extended Amortizations

The widespread adoption of 35-year mortgages has significant social and economic ripple effects.

Housing Market Volatility: Understand how extended amortizations can contribute to housing market volatility and potential bubbles.

Household Debt Levels: Analyze the impact of increased household debt levels on consumer spending, economic growth, and financial stability.

Intergenerational Wealth Transfer: Consider how extended amortizations can impact intergenerational wealth transfer and the distribution of wealth.

Social Equity and Access to Housing: Explore the implications of extended amortizations on social equity and access to affordable housing.

Community Development: Understand how extended amortizations can impact community development and the availability of affordable housing in certain areas.

Continuous Financial Education

The financial landscape is constantly evolving, making continuous financial education essential.

Stay Informed: Stay informed about changes in mortgage regulations, interest rates, and investment opportunities.

Read Financial Publications: Subscribe to reputable financial publications and blogs.

Attend Financial Seminars and Workshops: Attend financial seminars and workshops to learn from experts.

Seek Professional Advice: Build relationships with trusted financial advisors, mortgage brokers, and tax professionals.

Online Courses: Take advantage of online courses to learn about advanced financial concepts.

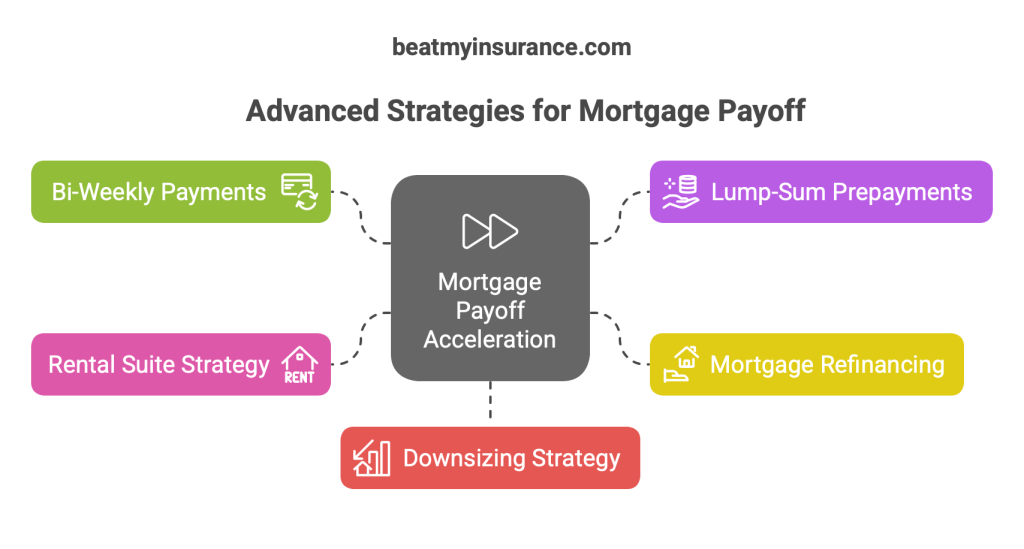

Strategies for Accelerating Mortgage Payoff

While a 35-year mortgage extends the repayment period, there are advanced strategies to accelerate payoff.

Bi-Weekly Accelerated Payments: Understand the impact of bi-weekly accelerated payments on your amortization schedule and total interest paid.

Lump-Sum Prepayments: Develop a strategic plan for making lump-sum prepayments, such as using bonuses, tax refunds, or inheritance.

Mortgage Refinancing: Explore advanced mortgage refinancing strategies, such as switching to a shorter amortization period or consolidating debt.•

Rental Suite Strategy: If permitted, adding a rental suite to your home can create additional income to accelerate payments.

Downsizing Strategy: Consider downsizing your home in the future to pay off your mortgage faster.

Building a Legacy of Financial Literacy

Beyond personal financial success, consider building a legacy of financial literacy.

Mentor Young Adults: Mentor young adults in your family or community about financial literacy.

Financial Literacy Organizations: Volunteer with organizations that provide financial education to underserved communities.

Create Educational Content: Create educational content, such as blog posts, videos, or podcasts, to share your financial knowledge.

Financial Literacy Initiatives: Support financial literacy initiatives through donations or advocacy.

Family Financial Meetings: Start having regular financial meetings with your family to discuss financial goals and strategies.

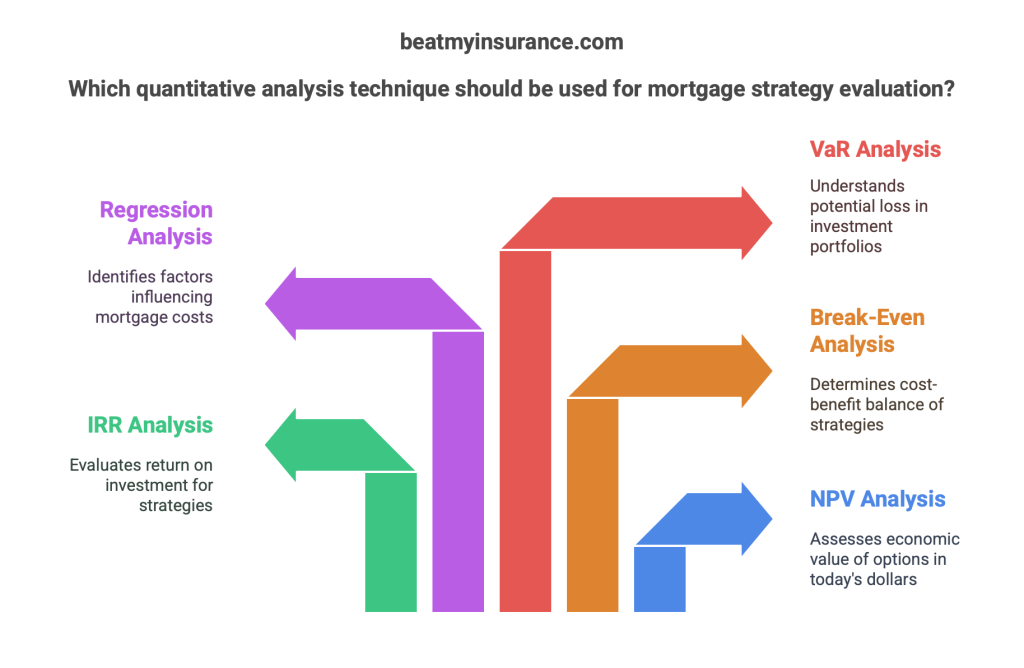

Quantitative Analysis of Mortgage Strategies

To move beyond qualitative assessments, let’s explore advanced quantitative analysis techniques applicable to mortgage decisions.

Net Present Value (NPV) Analysis: Apply NPV analysis to compare the present value of different mortgage scenarios, including various amortization periods, interest rates, and prepayment strategies. This allows you to assess the economic value of each option in today’s dollars.

Internal Rate of Return (IRR) Analysis: Use IRR analysis to evaluate the return on investment of different mortgage strategies, such as prepayments or refinancing. This can help you determine the most efficient use of your capital.

Break-Even Analysis: Conduct a break-even analysis to determine the point at which the benefits of a particular mortgage strategy, such as refinancing, outweigh the costs. This can help you make informed decisions about when to take action.

Regression Analysis: Employ regression analysis to identify the key factors that influence mortgage costs, such as interest rates, inflation, and property values. This can help you make more accurate predictions and develop more robust financial models.

Value at Risk (VaR) Analysis: For those with investment portfolios, use VaR to understand the potential for loss related to mortgage decisions, especially when leveraging strategies like the smith manoeuvre.

Use of Leverage in Mortgage and Investment

Leverage can amplify both gains and losses, making it a powerful tool for sophisticated investors. (“Understanding Leverage in Investment: Amplifying Gains and Risks …”)

Debt Recycling: Explore advanced debt recycling strategies, which involve using borrowed funds to invest in income-producing assets, while simultaneously paying down non- deductible debt.

Margin Lending: Understand the risks and rewards of margin lending, which allows you to borrow against your investment portfolio to finance mortgage payments or other expenses.

Real Estate Leverage: Analyze the optimal level of leverage for real estate investments, considering factors such as rental income, property appreciation, and interest rates.

Option Strategies: For those with high-risk tolerance, explore option strategies, such as covered calls or protective puts, to manage mortgage-related risks.

Integration of Behavioral Economics into Mortgage Planning

Behavioral economics provides valuable insights into the psychological biases that influence mortgage decisions.

Hyperbolic Discounting: Understand how hyperbolic discounting, the tendency to prioritize immediate rewards over future rewards, can lead to suboptimal mortgage choices.

Framing Effects: Be aware of how framing effects, the way information is presented, can influence your perception of mortgage costs and benefits.

Cognitive Biases and Financial Advisors: Understand how cognitive biases can impact the advice you receive from financial advisors and learn to critically evaluate their recommendations.

Nudging and Financial Behavior: Explore how nudging, the use of subtle cues to influence behavior, can be used to promote better mortgage decisions.

Emotional Intelligence and Financial Decision-Making: Develop emotional intelligence to manage the stress and anxiety associated with long-term financial commitments.

The Impact of Global Economic Trends

Canadian mortgages are influenced by global economic trends, making it essential to understand the interconnectedness of financial markets.

Global Interest Rate Policies: Analyze the impact of global interest rate policies, such as those of the Federal Reserve and the European Central Bank, on Canadian mortgage rates.

Currency Fluctuations: Understand how currency fluctuations can impact the cost of imported goods and services, affecting inflation and mortgage affordability.

Geopolitical Risks: Assess the potential impact of geopolitical risks, such as trade wars and political instability, on the Canadian economy and mortgage market.

Commodity Prices: Analyze the relationship between commodity prices, such as oil and gas, and the Canadian dollar, which can influence mortgage rates.

Global Debt Levels: Understand the implications of rising global debt levels on financial stability and mortgage markets.

The Role of Environmental, Social, and Governance (ESG)

ESG factors are increasingly important considerations for responsible investors and homeowners.

Green Mortgages: Explore the benefits of green mortgages, which offer incentives for energy-efficient homes.

Socially Responsible Investing (SRI) and Mortgages: Consider the social impact of your mortgage decisions, such as supporting lenders that promote affordable housing.

Climate Change and Property Values: Assess the potential impact of climate change on property values and mortgage risks.

Sustainable Homeownership: Adopt sustainable homeownership practices, such as reducing energy consumption and waste.

Governance and Mortgage Lending: Evaluate the governance practices of mortgage lenders to ensure they are transparent and accountable.

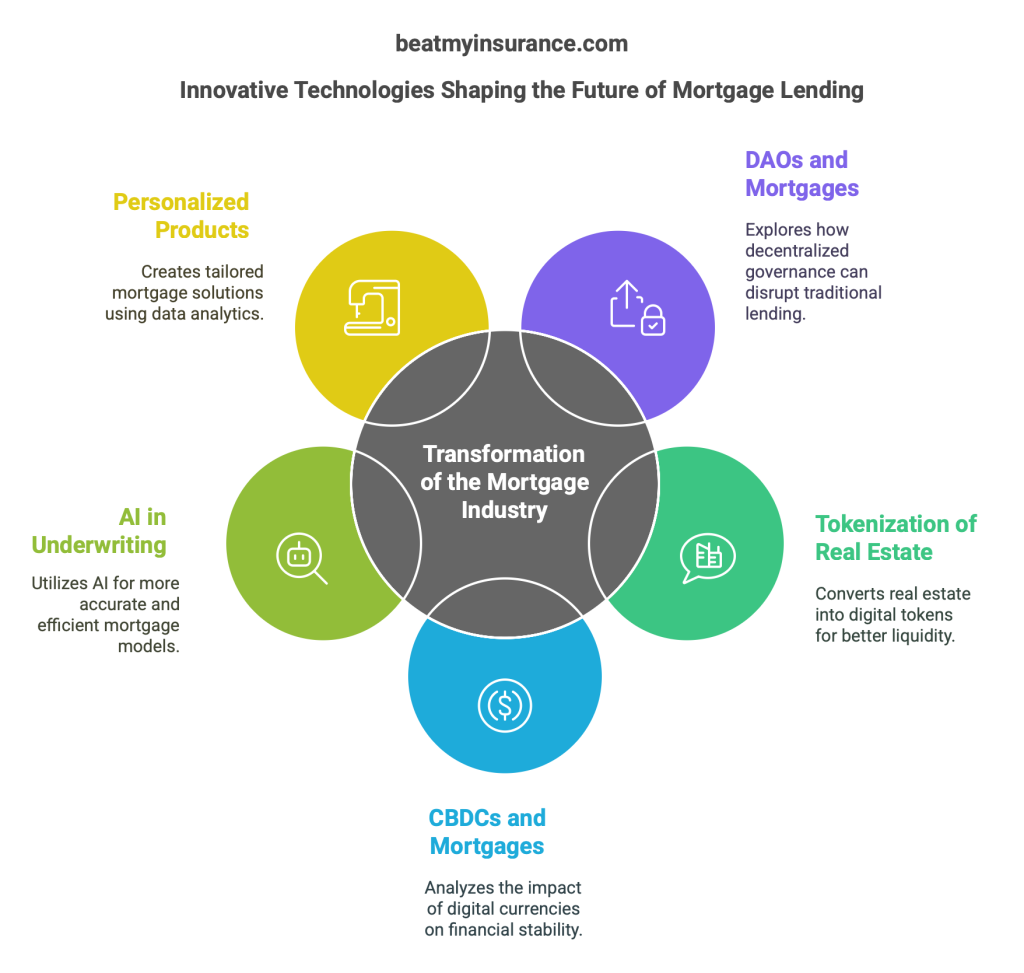

The Future of Mortgage Lending

The mortgage industry is undergoing rapid transformation, with the emergence of new technologies and business models.

Decentralized Autonomous Organizations (DAOs) and Mortgages: Explore the potential of DAOs to disrupt traditional mortgage lending by offering peer-to-peer lending and decentralized governance.

Tokenization of Real Estate: Understand how tokenization, the process of converting real estate assets into digital tokens, can increase liquidity and accessibility in the mortgage market.

Central Bank Digital Currencies (CBDCs) and Mortgages: Analyze the potential impact of CBDCs on mortgage lending and financial stability.

AI-Powered Mortgage Underwriting: Explore the use of AI and machine learning to develop more accurate and efficient mortgage underwriting models.

Personalized Mortgage Products: Understand how data analytics and AI are being used to create personalized mortgage products that cater to individual needs and preferences.

Wealth Creation and Mortgage Decisions

Wealth creation should be guided by ethical principles and a commitment to social responsibility.

Intergenerational Equity: Develop a deeper understanding of the ethical implications of intergenerational equity and how mortgage decisions can impact future generations.

Financial Inclusion and Access to Credit: Consider the ethical implications of financial inclusion and access to credit, especially for marginalized communities.

Responsible Lending Practices: Support lenders that adopt responsible lending practices and promote financial literacy.

Philanthropic Strategies: Integrate philanthropic strategies into your financial planning to give back to your community and support social causes.

Ethical Investing and Mortgage Decisions: Align your investment portfolio with your ethical values and consider the social and environmental impact of your mortgage decisions.

Personalized Financial Philosophy and Mortgage Strategy

Your mortgage strategy should be aligned with your personal financial philosophy and long-term goals.

Define Your Values and Priorities: Identify your core values and priorities, and ensure your mortgage decisions reflect them.

Create a Financial Mission Statement: Develop a financial mission statement that outlines your long-term financial goals and aspirations.

Build a Financial Team: Assemble a team of trusted financial advisors, mortgage brokers, and tax professionals to support your financial journey.

Practice Mindfulness and Gratitude: Cultivate mindfulness and gratitude to manage the stress and anxiety associated with long-term financial commitments.

Embrace Lifelong Learning: Commit to lifelong learning and continuous improvement in your financial knowledge and skills.

The Art of Negotiation in Mortgage Transactions

Negotiation skills are essential for securing favorable mortgage terms and minimizing costs.

Understanding Lender Incentives: Develop a deep understanding of lender incentives and motivations to negotiate more effectively.

Leveraging Data and Analytics: Use data and analytics to support your negotiation arguments and demonstrate your creditworthiness.

Building Rapport: Establish rapport with lenders and brokers to create a positive negotiation environment.

Mastering Negotiation Tactics: Learn and apply advanced negotiation tactics, such as anchoring, framing, and reciprocity.

Knowing Your Walkaway Point: Determine your walkaway point and be prepared to walk away from a deal if it doesn’t meet your needs.

Building a Resilient Legacy Through Financial Stewardship

Your mortgage decisions should be part of a broader strategy for building a resilient legacy.

Estate Planning: Develop a comprehensive estate plan that includes wills, trusts, and powers of attorney.

Succession Planning: Plan for the succession of your assets and businesses to future generations.

Family Wealth Management: Establish a family wealth management strategy that promotes financial literacy and responsible stewardship.

Philanthropic Legacy: Create a philanthropic legacy that reflects your values and supports causes you care about.

Mentoring and Empowerment: Mentor and empower future generations to become financially literate and responsible stewards of their resources.

Conclusion

The decision to opt for a 35-year mortgage requires a comprehensive understanding of its implications. By engaging in advanced financial planning, leveraging technology, understanding the psychological aspects, and building a resilient financial portfolio, you can make informed decisions that align with your long-term financial goals and create a lasting legacy.

Remember that financial literacy is a lifelong journey, and continuous learning is essential for navigating the complexities of the modern financial landscape

Here is the Mortgage Penalty Calculator, where you can easily and simply input your information, this will help you calculate the right mortgage for you and your family and help you save as getting a mortgage is a huge and difficult discussion and can affect the way you live mentally and financially.

So using BMI calculator will help you and this is your one-stop course that gives you an estimate of today’s current financial interest rates, inflation, and the economy as a whole.

Leave a Reply