American tariffs on Canadian exports, including a 25% tariff imposed by U.S. President Donald Trump, are driving up costs and could lead to higher insurance premiums for Canadians.

In response, Justin Trudeau, the prime minister of Canada, declared instantaneous countermeasures and imposed tariffs on $30 billion worth of American goods. The list of affected goods includes food items like meat and poultry, alcoholic beverages, various plastics, rubber materials, construction products such as wood panels and flooring, textiles, household appliances, machinery, and even vehicles, aircraft, and weaponry.

Further complicating the situation, Trump has declared a 25% tariff on all steel and aluminum imports, including those from Canada, set to take effect on March 12. With the cost of an average car rising by almost $3,000 and bigger SUVs possibly seeing a rise of up to $9,000, analysts warn this could greatly increase vehicle prices.

Targeting another $125 billion in U.S. imports, Trudeau also described plans for further retaliatory tariffs in three weeks. Canada also plans to contest U.S. tariffs using legal channels including the U.S.-Mexico-Canada Agreement (USMCA) and the World Trade Organization (WTO).

Trudeau underlined that as long as the United States keeps its own tariffs, Canada’s tariffs will stay in place; further non-tariff policies could be introduced in cooperation with provincial and territory leaders.

Rising Insurance Costs

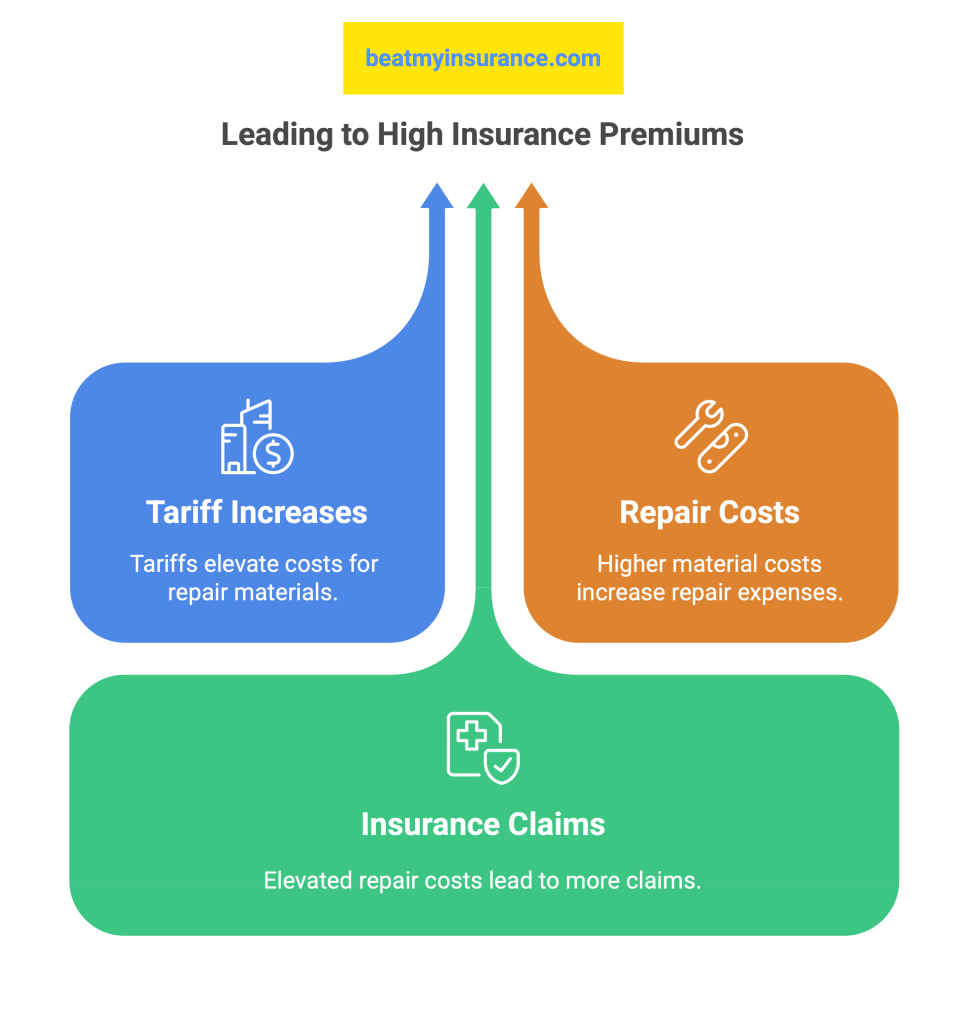

The Canadian insurance sector is bracing for the economic impact of these American tariffs. Industry experts warn that higher costs on imported materials needed for home and vehicle repairs will likely lead to increased claims expenses, which could translate to higher insurance premiums for consumers.

“American tariffs will increase costs for materials used in repairing and replacing homes, vehicles, and businesses, ultimately affecting insurance claims and leading to higher premiums,” the Insurance Bureau of Canada (IBC) stated.

Although the full extent of these effects is still unclear, the interconnected nature of the North American auto supply chain makes auto insurance particularly vulnerable, while home insurance could also see a rise in premiums due to the rising costs of building materials.

To mitigate these impacts, insurers may seek alternative suppliers to reduce reliance on American goods. However, the general expectation remains that claims costs across all lines of property and casualty (P&C) insurance will be affected, potentially leading to increased premiums for consumers.

Which Premiums Will Rise First?

According to Fitch Ratings, property insurance premiums will be the first to reflect these tariff-induced price increases. Unlike auto insurance, which is subject to government regulation in provinces like Ontario, home and commercial property insurance rates can be adjusted more quickly to account for rising costs.

“Home insurance premiums are not regulated by a central authority, meaning insurers can react more swiftly to changes in claims expenses,” Fitch noted. The trade war’s impact will likely exacerbate existing insurance cost pressures, including premium hikes driven by inflation, increased auto theft rates, and the record $8.9 billion in natural catastrophe-related losses Canada experienced last year.

While property insurance premiums could rise relatively quickly, auto insurance increases may take longer to materialize. Regulatory oversight in provinces like Ontario means that insurers must justify and submit proposed rate hikes for approval, a process that can take several months. Even after approval, consumers may not see changes until their policies come up for renewal, potentially delaying tariff-driven premium increases by a year or more.

Regulators will also have to consider the broader economic impact of these premium increases. A report from KPMG highlights the challenge provincial insurance regulators face in balancing necessary rate hikes with consumer affordability concerns, as Canadians already struggle with inflation and rising costs across multiple sectors.

As the trade war unfolds, both governments and businesses will be closely watching how American tariffs affect consumers. For Canadian insurance policyholders, the coming months could bring significant changes to their coverage costs, with home and auto insurance likely to feel the brunt of these economic shifts.

US Tariffs Impact Canadian Car Insurance

Prepare for Price Increases

Canadian car owners should brace for potential financial strain as new U.S. tariffs are set to take effect in March 2025. These American tariffs, targeting vehicles and auto parts, are projected to drive up costs across North America. For Ontario residents already juggling homeownership expenses, now is an ideal time to reassess insurance coverage.

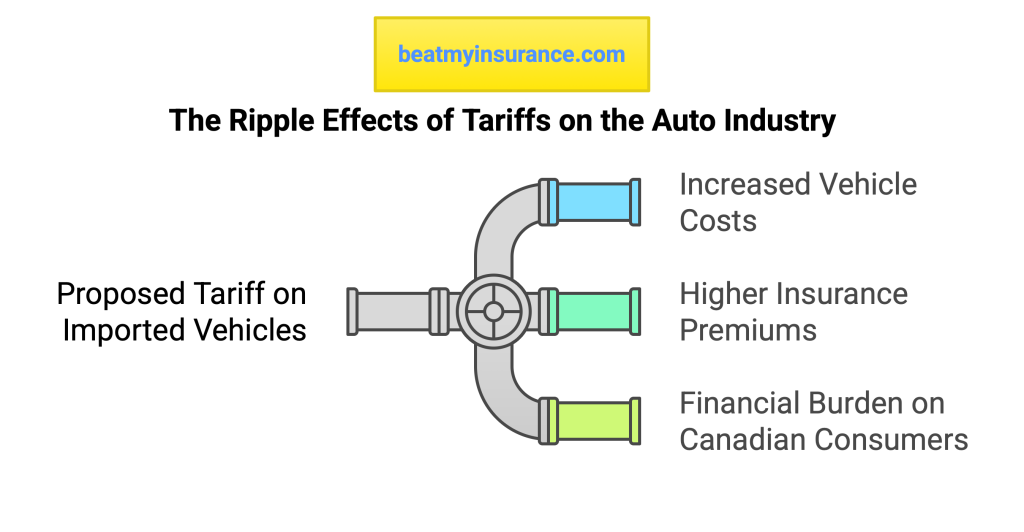

The Impact of a 25% Tariff

The proposed 25% tariff on imported vehicles and auto parts is expected to increase costs across the industry. As a result, insurance premiums in Canada are likely to follow suit. Analysts predict that new car prices in the U.S. could rise by approximately $3,000, potentially leading to an even greater financial burden for Canadian consumers.

Insurance Rates Are Already Climbing

Even before these American tariffs take effect, car insurance rates have been steadily increasing:

- Ontario drivers currently pay an average of $2,006 per year.

- This marks a 20% rise since October 2022.

- Across Canada, rates climbed 8.8% between October 2023 and October 2024.

- The previous year saw a 4.6% increase in rates.

- 2024 has recorded some of the sharpest rate hikes in recent years.

Contributing Factors to Higher Insurance Costs

In addition to trade tariffs, increasing incidents of auto theft have been a major contributor to rising insurance premiums:

- Auto theft claims in Canada reached $1.5 billion in 2023—a 254% surge since 2018.

- Ontario alone accounted for over $1 billion in theft claims in 2023, a 524% increase from 2018.

- These increases add approximately $130 to the average Ontario driver’s annual insurance premium, regardless of whether their car was stolen.

Industry professionals are raising concerns over the ripple effect of these American tariffs. Kevin Fujita, co-owner of CSN Kustom in Alberta, notes that rising costs will be passed on to consumers and insurance providers alike. Meanwhile, Aaron Sutherland from the Insurance Bureau of Canada warns that the 25% tariff will inevitably inflate auto insurance premiums due to costlier vehicle repairs and replacements.

Why Tariffs Affect Insurance Premiums

The connection between vehicle costs and insurance rates is clear:

- Higher Replacement Costs: More expensive vehicles lead to increased replacement expenses for insurers.

- Rising Repair Costs: Higher prices for auto parts will drive up repair bills.

- Premium Adjustments: Insurers will likely raise premiums to offset these heightened costs.

If you own a home or are planning to buy one, securing adequate insurance coverage is essential to safeguard your financial well-being.

How to Save on Car Insurance

Despite these financial pressures, there are effective ways to manage your insurance expenses:

- Compare Providers: Different insurance companies offer varying rates—shopping around can help secure a better deal.

- Bundle Policies: Combining auto and home insurance can lead to significant savings.

- Adjust Your Deductible: Opting for a higher deductible may reduce monthly premiums, but ensure it aligns with your financial situation.

Looking Ahead

The auto insurance landscape is rapidly changing, with new technologies and economic factors influencing rates. Staying informed can help you make smarter financial decisions and identify potential savings opportunities.

Take Charge of Your Insurance Costs

Now is the time to take action. Speak with your insurance provider about available coverage options, compare policies, and stay ahead of rising costs. Whether managing a mortgage or protecting your vehicle, being proactive is key to maintaining financial security.

How BeatMyInsurance.com Can Help

BeatMyInsurance.com eases the process by allowing you to compare multiple quotes from multiple brokers—all while staying anonymous until you accept a quote. This saves you time, protects your privacy, and ensures you find the best coverage at the most competitive price.

Don’t wait until rising premiums catch you off guard—take steps now to safeguard your finances and ensure you’re getting the best insurance coverage possible.

Ontario Insurance Costs May Rise

According to Business Insurance America, this is how American tariffs could drive up Ontario home and auto insurance costs:

Ontario homeowners and drivers may soon see higher insurance premiums due to newly imposed US tariffs on Canadian goods. Digital insurance marketplace rates.ca warns that rising material costs—particularly in the automotive and construction sectors—could have a ripple effect on insurance rates.

Starting March 12, a 25% tariff on Canadian steel will come into effect as part of a broader US strategy to protect its domestic steel industry. However, this move is expected to increase the cost of producing vehicles and constructing homes in Canada, potentially leading to pricier insurance claims and, ultimately, higher premiums.

Why Insurers Are Paying Close Attention

The Insurance Bureau of Canada is keeping a close watch on the situation, as the rising costs of materials could directly impact claim expenses. Since insurers base their rates partly on the cost of repairing or replacing damaged homes and vehicles, any significant increase in these expenses is likely to be passed on to policyholders.

Daniel Ivans, an insurance expert and licensed broker at RATESDOTCA, explains that although the full impact of the American tariffs will take time to unfold, consumers should be prepared for potential increases in insurance costs.

Canada’s Response to US Tariffs

In retaliation, the Canadian government has announced its own set of counter-tariffs on US-made products. Prime Minister Justin Trudeau has called the US decision “unjustified” and is implementing a 25% tariff on approximately CA$30 billion worth of American goods. If the US does not reverse its stance, an additional round of tariffs will take effect in three weeks, covering CA$125 billion worth of products, including cars, trucks, steel, and aluminum.

While the long-term effects of these American tariffs on the Ontario insurance market remain uncertain, experts agree that any increase in manufacturing and construction costs will likely contribute to higher insurance rates soon. Consumers should stay informed and prepare for potential changes in their premiums.

New tariffs introduced by U.S. President Donald Trump on March 4, 2025, are expected to significantly impact the Canadian group insurance sector, according to industry experts.

At the Group Conference hosted by the Insurance Journal Publishing Group on February 27, professionals discussed the potential effects, even as uncertainty loomed over whether the U.S. would move forward with the tariff measures.

The Impact on Prescription Drug Costs

The pharmaceutical industry is likely to feel the effects of these American tariffs. Since many medications pass through multiple countries before reaching Canadian pharmacies, added costs could drive up drug prices.

Éric Trudel, Executive Vice President at Beneva, noted that 40% of Canada’s medications originate from the U.S., while U.S. pharmaceutical companies rely on overseas suppliers for about 30% of their drugs. With the U.S. imposing a 10% tariff on imports from Asia—recently raised to 20%—and the Canadian dollar already weaker in comparison, this could lead to a 5% increase in drug costs. If Canada responds with its tariffs, the impact could be even greater.

Marie-France Amyot, Vice-President at Desjardins Insurance, emphasized the need for insurers to take a proactive approach. “We must ensure cost controls are in place, secure good agreements with pharmaceutical companies, and make certain that the right medications are provided under the right conditions,” she said.

Dental Costs Could Rise

American tariffs may also affect dental insurance. Many dental tools and equipment come from the U.S. and Europe, meaning costs could rise, potentially leading to higher insurance claims.

In Quebec, dental care costs traditionally follow the Régie des rentes du Québec (RRQ) index. However, recent trends show an accelerated increase. The Association des chirurgiens dentistes du Québec raised its rates by 4% in January, while the RRQ index only increased by 2.6%. Similarly, in Ontario, dental fees rose by 2%, aligning more closely with inflation.

Disability Insurance: Differing Opinions

Experts had mixed views on how American tariffs might impact disability insurance claims.

Amyot suggested that economic uncertainty often discourages employees from leaving their jobs, even when facing higher stress levels. Charles St-Laurent, Regional Vice-President at Medavie Blue Cross, agreed that disability claims may not rise in the short term but could increase if the economy slows down. He noted that during times of layoffs, employees may seek disability leave as an alternative to job loss.

Trudel, however, argued that in small and medium-sized businesses (SMEs), employees might hesitate to take disability leave due to job security concerns. Meanwhile, layoffs will reduce the number of contributors to group insurance plans, potentially driving up costs for remaining members.

Potential Job Market Shifts

Despite these concerns, actuary Jean-Guy Gauthier of CQFD Actuariat remained optimistic. He believes Canadian businesses will adapt by adjusting their offerings or expanding into new markets. In his view, benefits packages could become even more valuable as employers seek to attract and retain talent.

Travel Insurance and Changing Consumer Behavior

The impact on travel insurance is uncertain. Some experts believe that American tariffs could increase costs for insurers, particularly for policies covering trips outside North America. Others suggest that more Canadians may opt to travel domestically rather than to the U.S., which could offset cost increases in the short term.

Some airlines have already adjusted their flight schedules in anticipation of fewer Canadian travelers heading to the U.S.

Insurers Must Adapt

Given these challenges, industry leaders stress the importance of insurers taking an active role in managing costs and supporting plan sponsors.

Amyot emphasized that insurers must work closely with clients to ensure long-term sustainability. St-Laurent echoed this sentiment, recalling how insurers provided flexibility during the pandemic by extending coverage and allowing delayed premium payments.

Gauthier believes that advisors should take this opportunity to strengthen their client relationships. “Understanding our customers’ specific needs is key,” he said. “They may need aggressive renegotiations on their renewal, or they might be looking for reassurance during uncertain times.”

Ultimately, he sees change as an opportunity for insurers to demonstrate their value and adaptability.

Frequently Asked Questions

How would you define a tariff?

A tariff is a fee that a government places on imported goods or services. This charge makes foreign products more expensive and helps generate revenue for the country enforcing it.

Is a tariff considered a form of taxation?

Yes, a tariff is a kind of tax. It not only brings in money for the government but also helps local industries by making foreign goods less competitive. Additionally, tariffs can be used as a political tool in international trade.

Do tariffs directly impact consumer costs?

Yes, tariffs increase the price of imported products, which often results in consumers paying more for goods and services. Items like groceries, fuel, and other everyday necessities may see price hikes in Canada due to these trade policies.

What does the term “tariff trade war” mean?

A tariff trade war occurs when countries impose tariffs on each other’s imports in response to trade disputes, leading to escalating economic tensions.

In what ways do tariffs influence consumers?

By increasing the price of imported goods, tariffs make everyday products more expensive. For instance, Canadian shoppers may pay more for fruits imported from the U.S. Similarly, tariffs affecting trade with China, Mexico, and the U.S. could lead to higher prices on cars, electronics, clothing, toys, and food.

What are some downsides of tariffs?

Tariffs can lead to higher costs for consumers, potentially limiting their spending and slowing down economic growth.

Can a country “win” a trade war?

Trade wars rarely have clear winners, as they can negatively impact all sides. However, countries may attempt to strategically impose tariffs on select imports to protect domestic businesses and reduce reliance on specific trade partners.

Are there any advantages to a trade war?

While trade wars have drawbacks, they can also shield domestic industries from foreign competition and help sustain jobs. Higher costs on imports may push consumers to buy locally, boosting demand for domestic products. Additionally, trade disputes can encourage nations to explore new trade partnerships.

Leave a Reply