Your child just passed their G2 test. They’re thrilled. You’re proud (and maybe a little terrified). But before they take the family car for a spin, there’s one huge thing you can’t skip: adding them to your car insurance.

It’s not just a good idea. In Canada, it’s a legal requirement—and skipping it could raise your car insurance cost or even lead to denied claims.

Let’s break down what this means, how much it’ll cost, how to save, and what parents really need to know when it comes to insuring their teenage driver.

Also read: New mortgage rules in Canada: What Changed?

#1 Thinking It’s Unnecessary

Yes, absolutely. As soon as your child gets their G2 license, they must be listed on your policy—even if they’re only driving occasionally. Every licensed driver in your household needs to be disclosed to your insurer.

Why it matters:

- If your teen gets in an accident and isn’t listed, your claim could be denied.

- You could be personally liable for damages—which can easily hit over a million dollars in injury claims alone.

- Not disclosing them is considered non-disclosure, and it could affect your entire policy.

- If your adult child still lives with you and uses your car now and then, they must be listed on your policy—typically as a secondary or occasional driver. It’s based on residency and access to the vehicle, not just age.

Optional: Using an Exclusion Form

Some parents choose to formally exclude their child from the insurance policy using a legal document called an exclusion form. This means the child is not allowed to drive the insured vehicle under any circumstance, and if they do, there will be no coverage. This approach may help keep car insurance costs lower, but it should only be used if you’re certain the child won’t be driving the car.

#2 Not Being Prepared of The Costs

Here’s the not-so-fun part: your car insurance costs will go up. In Canada, car insurance usually costs between $1,300 and $1,800 per year. But for teen drivers, it’s much higher—often two to three times more.

Suppose you live in North York, Ontario, adding an 18-year-old to your policy as an occasional driver could cost anywhere from $500 to $3,000 per year. But it depends on:

- Your insurer

- Where you live (urban vs rural)

- Your teen’s driving history

- The type of vehicle they’ll be using

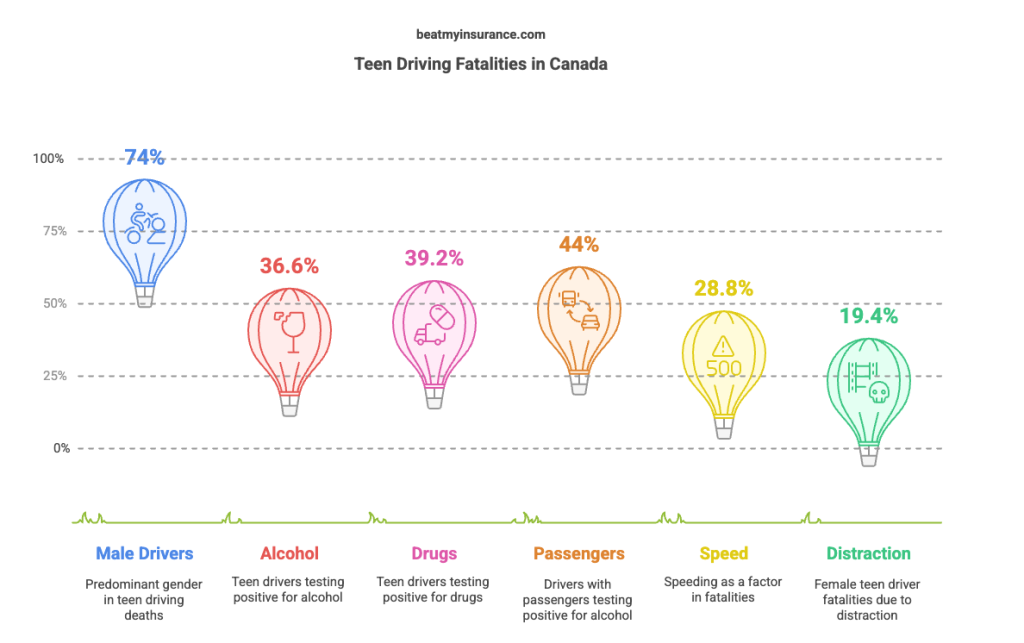

Male drivers aged 16–19 typically face the highest premiums, but don’t worry—there are ways to cut that down.

But why so expensive, you might ask? They are just teens! That’s exactly why!

Teen car insurance in Canada is expensive because young drivers are more likely to get into accidents. Their lack of experience, riskier driving habits, and higher chances of speeding make them high-risk for insurers. As a result, premiums for teen drivers are much higher than average. Here are some stats –

#3 Thinking high premiums are the only option!

What if we tell you paying high car insurance costs isn’t the only way? Here’s how-

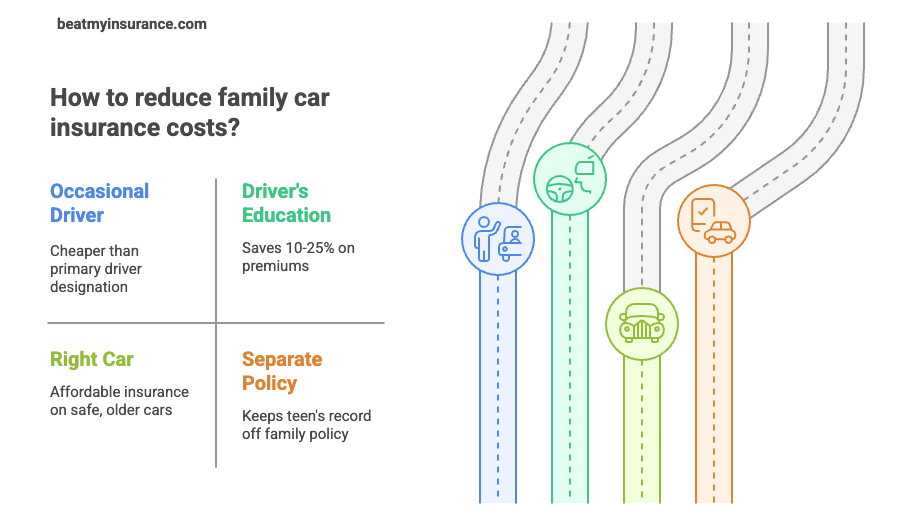

Add Them as an Occasional Driver

If your teen won’t be driving every day, this designation is much cheaper than making them the primary driver.

Get Driver’s Education

A government-approved driving course can save you 10–25% on premiums.

Use the Right Car

Avoid flashy sports cars or anything new and expensive. Insuring a teen on a safe, older, lower-value car is way more affordable. The car you choose plays a big role in your insurance premiums. Find out which car can help keep your car insurance cost low.

Note: If your teen is driving the newest or most expensive car in the house, your insurer may assume they’re the primary driver unless you tell them otherwise.

Consider a Separate Policy

If your teen owns their own vehicle, a separate policy keeps their accidents and tickets off your record. Just be aware: it may cost more initially, but can be smart in the long run.

Explore Telematics

Some insurance companies offer apps or devices that track driving habits (braking, speed, time of day). Safe driving = discounts.

Bundle Up

Home + auto with the same provider? You could save 15–20%. Try apps like beatmyinsurance.com to save time and let brokers come to you instead!

Winter Tires & Anti-Theft Devices

These can earn you extra discounts in many provinces.

Maintain a Good Academic Record

Teens with a B average or higher can qualify for good student discounts.

#4. Not Knowing About These Factors

- Territory Rating: Living in a city = higher premiums. Rural = less risk, lower rates.

- Credit Score: In some areas, your credit score (or the family’s) can influence rates.

- High-Value Homes: Own a home worth over $1M? Some insurers offer better packages with lower auto rates.

- Multiple Vehicles: Households with more than one car can qualify for multi-car discounts.

- Deductibles: Choosing a higher deductible lowers your monthly rate, but means you’ll pay more if there’s a claim.

- Advanced Training: Courses beyond basic driving school may qualify for even more discounts.

- Annual Reviews: Always review your policy yearly—your teen’s experience, age, and driving record can lead to rate changes.

- G2 to G: Once your teen gets their full G license, notify your insurer—it could lower their premium.

#5 Risk Management

Some families buy a cheap, older car and insure it with a minimum coverage policy just for their teen. This separates risk and often encourages safer habits.

Why?

- When teens have their own policy, they tend to drive more carefully—because they know one ticket means years of higher rates.

- At-fault accidents or multiple violations can make your teen a high-risk driver, and insurers may drop or deny coverage.

- A clean driving record leads to gradually lower premiums over time.

#6. Not Updating Policy for Absent Teen

If your child moves away for college and doesn’t have regular access to a car, ask your insurer about “away-from-home” discounts—especially if they’re over 100 km away.

Some companies even offer seasonal policies for part-time student drivers.

#7 Accident Forgiveness

If your policy includes accident forgiveness, your teen’s first at-fault accident may not raise your premium. It’s a valuable option to consider with new drivers.

What Is Accident Forgiveness in Car Insurance?

Accident forgiveness is an optional feature offered by many car insurance companies. It means your insurer won’t raise your rates after your first at-fault accident. It’s a way to protect your premium from going up just because of one mistake—especially helpful for drivers with a clean record.

How It Works

- If you’re in an at-fault accident and you have accident forgiveness on your policy, your insurer will “forgive” the crash and your premium won’t go up because of it.

- It only applies to the first at-fault accident and is usually available to drivers with no previous claims or serious driving violations.

- You’ll still have to pay your deductible for any damage, but your rates won’t spike.

- Accident forgiveness isn’t automatically included—you need to request it and it often costs extra.

- You must already have the coverage before the accident happens. You can’t add it after.

Who Qualifies for Accident Forgiveness?

Not everyone can get accident forgiveness. Insurance companies typically require:

- A clean driving history with no at-fault accidents or serious violations for several years (often 6).

- An active policy with the company.

- That the vehicle is for personal use—not commercial.

Some insurers include it in their standard coverage, while others offer it as an add-on (known as an “endorsement”). If you switch companies after an accident, the forgiveness usually doesn’t carry over.

#8 Policy Lapse!

Gaps in insurance history = higher future rates. Even if your teen isn’t driving full-time, keeping continuous coverage helps in the long term.

Also: Don’t miss payments. If a policy gets cancelled for non-payment, your teen will face much higher premiumswhen reapplying.

#9 Not Planning Ahead

Once your teen is older, gainfully employed, or owns their own car, it might be time to transition them to their own policy. Done right, this move:

- Helps them become financially independent

- Keeps your policy clean

- May unlock new discounts or bundles

Having a strategy for that shift saves money in the long run.

Final Thoughts

Yes, adding your teen to your car insurance might sting a little financially—but not doing it can hurt a whole lot more.

The key is to stay informed, use discounts wisely, and shop around for the best deal.

Tip: Insurance quotes for teens can vary a lot between companies.

Before locking into anything, compare rates from multiple providers to see who offers the most value.

Leave a Reply