Although life insurance is a necessary financial tool providing security and peace of mind, many people are not aware of its advantages, expenses, or uses. Often by postponing or not purchasing life insurance at all, uninformed people put their loved ones at financial risk. If you’re wondering, “Is life insurance worth it?” this article busts the most common misconceptions about it and clarifies, backed by data and expert opinions, how it works.

Misconception #1: “I Don’t Need Life Insurance If I’m Young and Healthy”

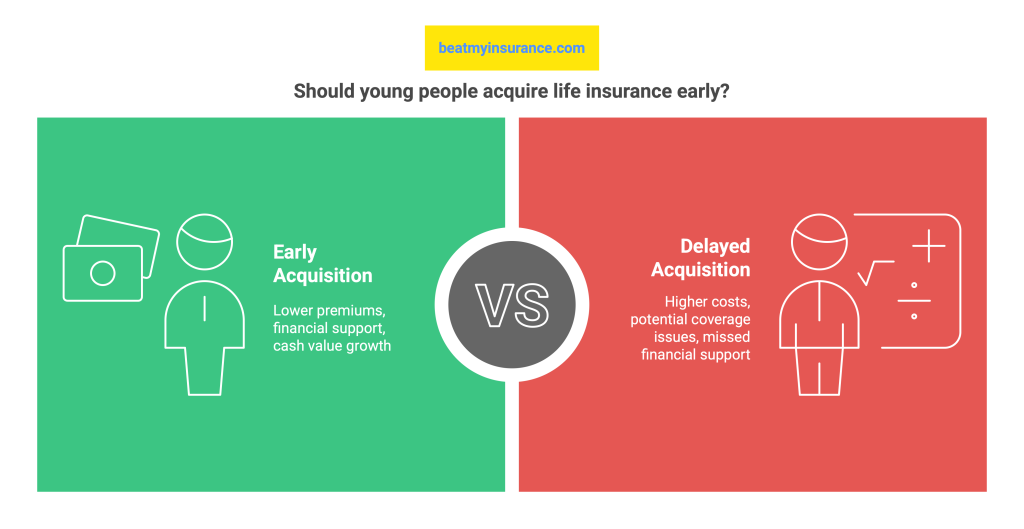

Many young people believe they need life insurance only once they are older or have dependents. Still, there are several reasons why early acquisition of life insurance can be beneficial.

- The younger and healthier you are will help to lower your premiums. Over time, being locked in a lower rate will help you save money.

- Any time can bring unexpected health issues that might make coverage later in life difficult or more costly.

- Even without dependents, life insurance can assist your family financially by helping to pay debt, cover funeral expenses, and support them overall.

Certain life insurance products, such as whole or universal life insurance, build cash value over time that can be borrowed against or withdrawn.

Supporting Information:

- LIMRA reports that almost half of millennials overstate the cost of life insurance by five times its actual cost.

- According to Life Insurance Marketing and Research Association (LIMRA), should the main wage earner die, 44% of American homes would experience financial difficulty within six months.

Misconception #2: “Life insurance is too expensive”.

One of the most common misconceptions is that life insurance is unduly costly. Actually, many times, life insurance is less expensive than most people believe. Age, health, coverage level, and type of policy all influence the cost of a policy.

Often the most reasonably priced choice, term life insurance offers coverage for a designated period—say 10, 20, or 30 years. Though generally more costly, permanent life insurance provides lifetime coverage and incorporates a cash value component.

Many insurance companies provide adaptable plans that fit varying budgets and financial requirements. Certain insurance companies provide discounts if you combine life insurance with either home or auto insurance policies.

Misconception #3: “I Have Life Insurance Through My Employer, So I Don’t Need Additional Coverage”

While employer-provided life insurance is a great benefit, it often has limitations:

- Insufficient Coverage: Many employer policies provide only one or two times your annual salary, which may not be enough to support your family in the long term.

- Lack of Portability: If you leave your job, you may lose your coverage.

- Limited Customization: Group life insurance policies typically offer minimal flexibility in terms of coverage amounts and beneficiary options.

- Employer Dependency: Relying solely on employer-sponsored life insurance means you may not have continuous coverage throughout your career.

For comprehensive financial protection, consider supplementing your employer-provided life insurance with an individual policy.

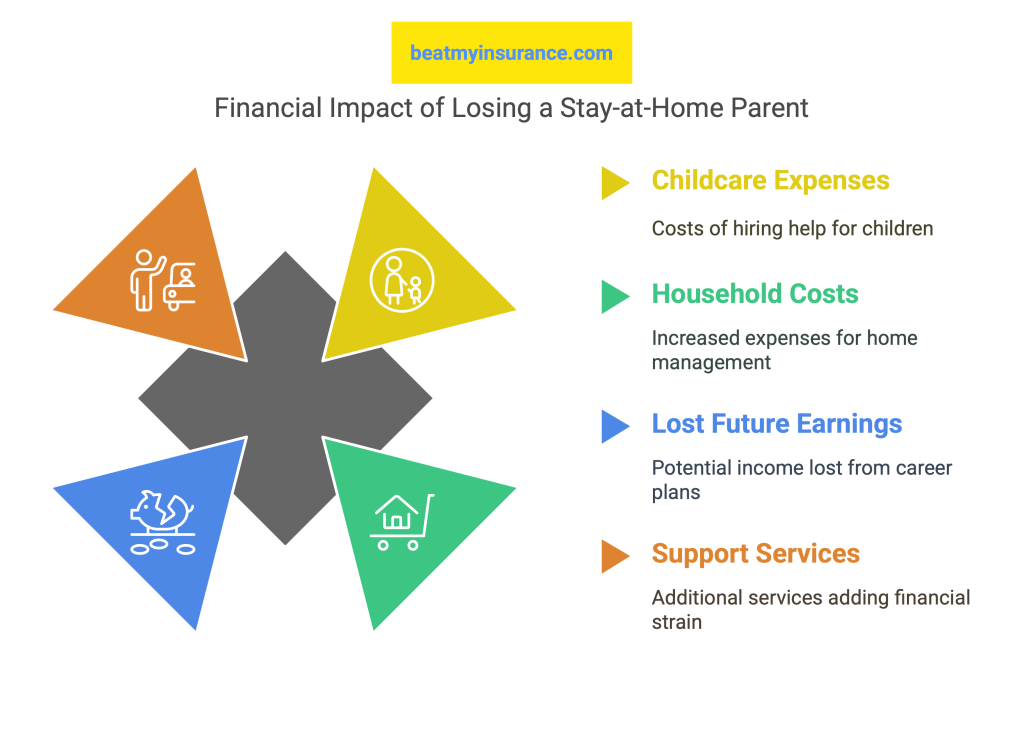

Misconception #4: “Stay-at-Home Parents Don’t Need Life Insurance”

Stay-at-home parents provide valuable services such as childcare, housekeeping, and meal preparation, which would be costly to replace. If a stay-at-home parent passes away, the surviving spouse may face significant financial burdens, including:

- Childcare Expenses: Hiring a nanny or enrolling children in daycare can be expensive.

- Household Costs: Increased expenses for meal preparation, cleaning, and household management.

- Lost Future Earnings: If the stay-at-home parent plans to return to work in the future, their potential income is lost.

- Support Services: Additional services such as tutoring, transportation, and home maintenance can add financial strain.

Supporting Data:

A 2022 study by Salary.com estimated that the value of a stay-at-home parent’s work equates to an annual salary of over $184,000.

The Bureau of Labor Statistics reports that childcare costs have risen by nearly 40% over the past decade, making financial planning essential for families.

Misconception #5: “Life Insurance Payouts Are Taxable”

Life insurance death benefits are generally not subject to federal income tax. Beneficiaries receive the payout tax-free, allowing them to use the funds for expenses such as funeral costs, debt repayment, and daily living expenses. However, there are exceptions:

- Estate Taxes: If the policyholder’s estate is large enough to be subject to estate taxes, the proceeds could be included in the taxable estate.

- Interest Earnings: If the insurance company holds the payout in an interest-bearing account, the interest earned may be taxable.

- Corporate-Owned Policies: In cases where a business owns a life insurance policy, certain tax implications may apply.

Consult a financial advisor to understand how life insurance fits into your overall estate planning strategy.

Front & Backlinks:

- For a detailed guide on choosing the right life insurance policy, visit LIMRA’s Official Guide.

- Read about the importance of financial planning at Investopedia.

- Learn about tax implications at IRS Life Insurance Guidelines.

Life insurance is an essential financial tool, yet many people avoid it due to myths and misconceptions. Understanding the truth about life insurance can help individuals make informed decisions to protect their families and financial futures.

Misconception #6: Life Insurance is Too Expensive

Fact: Many people overestimate the cost of life insurance. According to a 2022 study by LIMRA (Life Insurance Marketing and Research Association), more than 50% of Americans believe life insurance is three times more expensive than it actually is.

- Reality: A healthy 30-year-old non-smoker can obtain a $500,000 term life insurance policy for around $20–$30 per month.

- Research Insight: The Insurance Barometer Study by LIMRA found that cost misperception is a leading reason why people don’t purchase coverage.

👉 Source: LIMRA Insurance Barometer Study

Misconception #7: Life Insurance is Only for Death Benefits

Fact: Certain types of life insurance, such as whole and universal life policies, offer living benefits, such as cash value accumulation and borrowing options.

Examples of Living Benefits:

- Policy loans or withdrawals for emergencies, education, or retirement.

- Accelerated death benefits for terminal illnesses.

Research Insight: A 2023 Forbes Advisor report highlights that nearly 40% of whole-life policyholders use their policies to supplement retirement income.

👉 Source: Forbes – Benefits of Permanent Life Insurance

Misconception #8: It’s Difficult to Qualify for Life Insurance

Fact: Advances in underwriting and policy options have made life insurance more accessible. Even individuals with pre-existing conditions can find coverage.

- Simplified Issue & No-Exam Policies: Many insurers offer policies that do not require a medical exam.

- Guaranteed Issue Life Insurance: This option provides coverage regardless of health conditions, though premiums may be higher.

👉 Source: NerdWallet – Life Insurance for Pre-Existing Conditions

Is Life Insurance Worth It?

Life insurance is a crucial component of financial planning, yet many individuals delay or avoid purchasing coverage due to misunderstandings. By separating fact from fiction, you can make more informed decisions about protecting your loved ones.

If you’re still wondering, “Is life insurance worth it?”, consider this: life insurance offers peace of mind, financial security, and protection against unexpected hardships—all for a relatively low cost. If you haven’t reviewed your life insurance needs recently, now is a great time to start.

Next Steps:

✔️ Assess your financial needs and future obligations.

✔️ Compare different life insurance policies.

✔️ Speak with a licensed insurance advisor for personalized recommendations.

If you need Life Insurance, BeatMyInsurance.com is your “BEST CHOICE”. We provide you with a seamless experience for the buyer who can put their information in, stay anonymous, and have brokers compete for your business by providing you with the most competitive offer. It’s a free sign, and no credit card is required!

If you looking for Life Insurance and what an easy streamlined process is, then click on this link and get started today!