Investment properties are valuable assets that generate income and progressively increase wealth. They do, however, come with some inherent risks, like the possibility of property damage, tenancy issues, and legal liabilities.

You need to have adequate landlord insurance coverage to safeguard your investment against unforeseen circumstances. This blog explores the critical importance of insurance for investment properties using case studies, research, and expert opinions.

The Dangers of Investment Property Ownership

1. Property Damage and Natural Disasters

Natural disasters such as earthquakes, floods, fires, and hurricanes can have an impact on investment properties. In 2023, insured damage from severe weather amounted to $3.1 billion, according to the Insurance Bureau of Canada (IBC), highlighting the growing risk to property owners. (reference).

The frequency of climate-related disasters has increased over the last decade. According to a Canadian Climate Institute report, the frequency of extreme weather events has increased by 25% over the past decade. Without adequate landlord insurance, property owners risk suffering significant financial losses and potential property devaluation.

The Government of Canada’s Climate Change Report provides a thorough analysis of climate risks for property owners.

2. Hazards Associated with Tenants

Sometimes, whether on purpose or by accident, tenants can damage rental properties. According to the Canadian Real Estate Association (CREA), the average annual cost of property repairs resulting from damage caused by tenants is $2,500 for landlords. Financial strain can also result from problems like unpaid rent or legal disputes.

Legal troubles and evictions may make things even more difficult. According to a 2023 Landlord and Tenant Board of Ontario study, unpaid rent was a factor in more than 30% of landlord-tenant disputes, costing each landlord an average of $5,200 in lost revenue.

3. Concerns About Liability

Tenant safety is your responsibility as a property owner. Tenants or guests may file a lawsuit for damages and medical costs if they are hurt as a result of carelessness. You might have to pay thousands of dollars in settlements and legal fees if you don’t have landlord insurance.

Slip-and-fall incidents rank among the most frequent claims against landlords, according to the Insurance Information Institute, Medical and legal costs for a claim average $20,000.

To learn how to legally protect yourself, go to the Ontario Landlord and Tenant Board.

Insurance Types for Investment Properties

1. Insurance for landlords

Property damage, liability protection, and loss of rental income are all covered by landlord insurance. More comprehensive protection than typical homeowner’s insurance is provided by landlord insurance, which is especially made for rental properties.

2. Insurance for Liability

If a tenant or other third party is hurt on the property, liability insurance shields the landlord from lawsuits. A liability claim in the United States typically costs about $22,000, according to the Insurance Information Institute, highlighting the significance of coverage.

3. Insurance for Loss of Rental Income

Loss of rental income insurance reimburses you for lost rent while repairs are being made to your rental property if covered damage renders it uninhabitable. According to data from the Canadian Mortgage and Housing Corporation (CMHC), landlords may lose thousands of dollars annually as a result of vacancy-related losses.

4. Insurance for Earthquakes and Floods

Natural disasters like earthquakes and floods are often not covered by standard policies. Specialized coverage is required to guard against catastrophic losses if your property is situated in a high-risk area. Examine the Government of Canada’s risk assessment resources.

Only 40% of property owners in high-risk flood zones have flood insurance, according to a 2024 study by the Canadian Institute for Catastrophic Loss Reduction (ICLR), putting many at risk of experiencing extreme financial hardship.

The Effect of Not Having Insurance

According to a National Association of Realtors (NAR) study, uninsured property damage costs US real estate investors $9 billion on average every year. Furthermore, 40% of real estate investors suffered large financial losses as a result of insufficient insurance coverage, according to a 2022 study published by Canadian Real Estate Wealth magazine.

Visit Real Estate Wealth Canada for additional data on the risks associated with real estate investments.

Case Study: The Price of Not Being Insured

John owned a multi-unit rental property and was a Toronto real estate investor. An electrical problem in 2021 resulted in a fire that damaged $150,000 worth of property. He had to pay for all of the repairs out of pocket because he lacked landlord insurance. In addition, he lost $25,000 in rental income because his tenants had to relocate. His financial losses would have been negligible if he had acquired a comprehensive landlord insurance policy.

In a similar vein, a British Columbian real estate investor lost $200,000 after a flood destroyed his rental home. His investment plans were severely delayed since he was forced to use his personal savings to pay for repairs due to a lack of proper landlord insurance.

Legal Obligations and Adherence

1. Federal and Provincial Laws

Certain provinces require specific insurance coverage for landlords, depending on the area.

For instance, the Landlord and Tenant Board (LTB) of Ontario requires that landlords include information about insurance in rental agreements. On the LTB website, you can review the legal requirements.

2. Conditions for Mortgage Lenders

As a condition of financing, the majority of mortgage lenders demand that real estate investors carry insurance.

In the event of loss or damage, banks and other financial institutions want to safeguard their investments. Examine the Canada Mortgage Brokers Association’s and CMHC’s mortgage lending requirements.

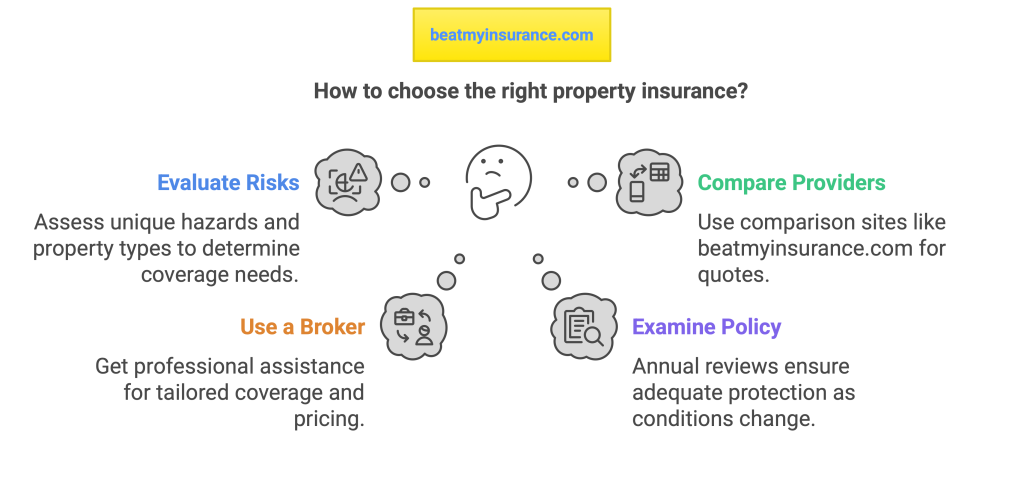

How to Pick the Appropriate Insurance Plan

1. Evaluate the Risks to Your Property

To ascertain the required level of coverage, consider potential risks such as hazards unique to a given location, the type of tenant, and the age of the property.

Use the risk calculator offered by Intact Insurance to get a free risk assessment tool.

2. Compare Several Providers

Read customer reviews, compare policy offerings, and conduct research on various insurance providers. Sites like beatmyinsurance.com help you compare multiple quotes all in one place!

3. Assist an Insurance Broker

Finding the ideal coverage for your needs at affordable prices and navigating the complexities of property insurance are tasks that a broker can assist you with. For licensed professionals, go to the Insurance Brokers Association of Canada.

4. Examine Your Policy Frequently

Reviewing your insurance policy once a year guarantees that you have enough protection as risks, market conditions, and property values change over time.

In conclusion

Investment properties need strong protection because they are important financial assets. Landlord insurance guarantees adherence to legal and lender requirements in addition to reducing financial risks.

Property investors can protect their capital, reduce losses, and guarantee long-term profitability by obtaining comprehensive landlord insurance coverage.

Try beatmyinsurance.com today, for FREE! All you need to do is sign up, post your listing, and let brokers come to you instead!

Leave a Reply