Latest Changes in the Canadian Housing Market

In Canada, the new mortgage rules look to guarantee financial stability, limit too-high debt, and keep the housing market in balance. These adjustments affect borrowers by changing amortizing periods, tightening qualifying criteria, and modifying affordability incentives. Prospective buyers and present homeowners must understand these rules if they are to make wise financial decisions.

The Canadian housing market is always changing thus, both present homeowners and prospective buyers should stay educated about new mortgage rules being proposed. The new mortgage regulations in Canada affect insured mortgages and affordability, influencing buyers’ access to finance. Whether you are investing in real estate, refinancing, or your first house, knowledge of these rules is absolutely vital.

Why Mortgage Rules Matter

Mortgage rules are implemented to ensure financial stability, curb excessive debt, and maintain a healthy real estate market. This means:

- Improve housing affordability.

- Strengthen risk management for lenders.

- Protect borrowers from overleveraging.

Key Changes in Mortgage Regulations

1. Stress Test for All Borrowers

A stress test for insured as well as uninsured mortgages has been created by the Canadian government Borrowers must thus prove they can afford payments should interest rates rise by qualifying at a rate higher than their actual mortgage rate. The qualifying rate is either the lender’s contracted rate plus 2% or the benchmark rate set by the Bank of Canada.

A report from the Bank of Canada found that the stress test has reduced risky borrowing by 20%, ensuring that homebuyers are financially stable even in uncertain economic conditions. However, it has also made homeownership less accessible for some lower-income buyers.

2. Tightening Insured Mortgage Requirements

For mortgages requiring insurance (typically those with a down payment of less than 20%), stricter guidelines apply:

- Borrowers must meet minimum credit score requirements.

- Properties must be owner-occupied (rental properties do not qualify).

- Maximum amortization for insured mortgages remains at 25 years.

Data from the Canadian Mortgage and Housing Corporation (CMHC) shows that insured mortgages now represent a smaller portion of total mortgage lending, indicating a shift towards higher down payments among buyers.

3. Changes in Mortgage Amortization Periods

For uninsured mortgages (down payments of 20% or more), the amortization period can extend to 30 years. However, insured mortgage amortization is capped at 25 years, limiting flexibility for some homebuyers.

According to Statistics Canada, longer amortization periods lead to lower monthly payments but higher overall interest costs, which could impact long-term financial stability.

4. Debt Service Ratio Limits

The Gross Debt Service (GDS) ratio and Total Debt Service (TDS) ratio restrictions ensure borrowers do not take on excessive debt:

- GDS ratio should not exceed 39% of gross income.

- TDS ratio must not exceed 44% of gross income.

A recent study found that 35% of mortgage applications are rejected due to high debt service ratios, emphasizing the importance of financial planning before applying.

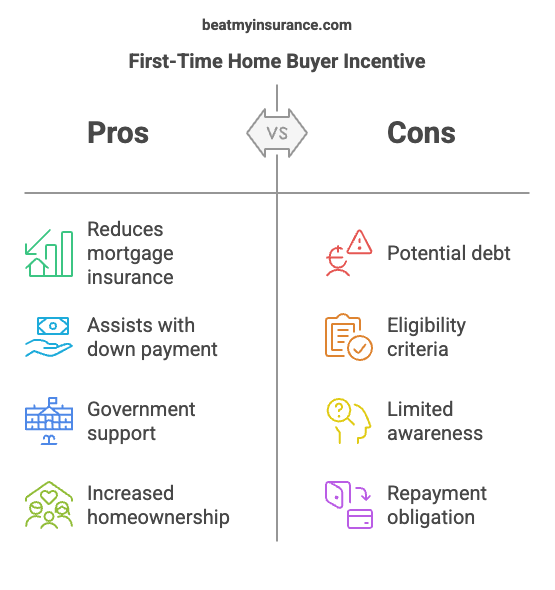

5. First-Time Home Buyer Incentive Adjustments

The government has adjusted its First-Time Home Buyer Incentive to provide more flexible options for affordability. This includes increased eligibility for households with higher incomes, allowing more Canadians to qualify for homeownership assistance.

Recent statistics indicate that 60% of first-time buyers who applied for the incentive were able to purchase homes they otherwise wouldn’t have qualified for.

How These Changes Impact Homebuyers

Affordability Challenges

With the stricter stress test and tighter mortgage requirements, some first-time homebuyers may find it harder to qualify for their desired property. Buyers may need to:

- Save for a larger down payment.

- Consider properties within a lower price range.

- Improve their credit score before applying.

A survey by the Canadian Real Estate Association (CREA) found that 45% of first-time buyers delayed their home purchases due to these affordability challenges.

More Competition in the Market

With more stringent mortgage regulations, demand for lower-priced homes may increase, leading to greater competition in certain segments of the market. Buyers must act strategically, securing pre-approvals and working with financial advisors to navigate the new landscape.

Interest Rate Considerations

The Bank of Canada’s interest rate trends play a crucial role in mortgage affordability. As rates fluctuate, mortgage payments for variable-rate holders can change, impacting overall housing costs.

In 2023, variable-rate mortgage holders saw an average increase of $250 per month in payments due to rising interest rates, making budgeting more critical than ever.

Different Types of Mortgages in Canada

Before choosing a mortgage, it’s important to understand the different types available in the market.

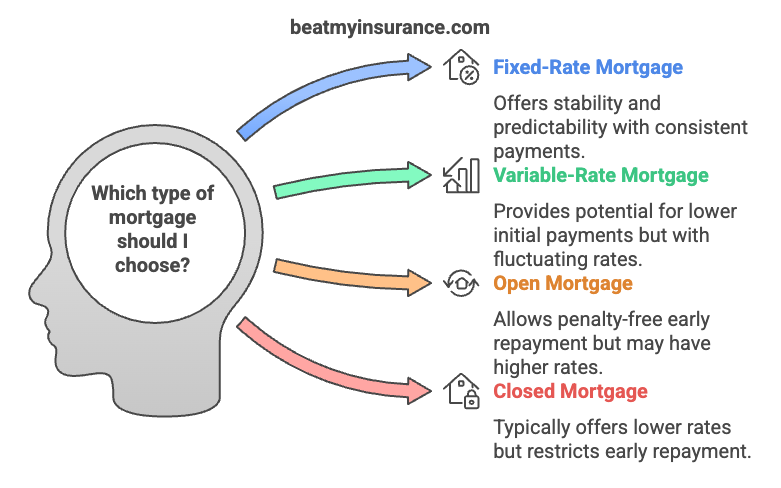

Fixed-Rate Mortgages

- The interest rate remains the same throughout the term.

- Provides stability and predictability.

- Suitable for buyers looking for consistent payments.

Variable-Rate Mortgages

- Interest rates fluctuate based on the market.

- Can result in lower initial payments, but there’s a risk of rate increases.

- Ideal for those comfortable with potential payment changes.

Open vs. Closed Mortgages

Open mortgages allow early repayment without penalties but often have higher rates. (“Samson Tella – Greater Toronto Area, Canada – LinkedIn”)

Closed mortgages have lower interest rates but limit prepayment options.

How to Prepare for the New Mortgage Rules

If you’re planning to buy a home, these steps can help ensure you’re financially prepared:

1. Assess Your Financial Health – Review your credit score, debts, and savings.

2. Save for a Larger Down Payment – A bigger down payment can help avoid mortgage insurance and reduce loan amounts.

3. Get Pre-Approved – Understanding what you qualify for helps in budgeting and house hunting.

4. Consult a Mortgage Professional – Expert advice can help in selecting the right mortgage product.

Why Mortgage Insurance Matters More Than Ever

- A Bank of Canada report found that 20% of borrowers failed the new stress test, highlighting the need for financial preparedness.

- The Canadian Mortgage and Housing Corporation (CMHC) states that insured mortgages now represent a smaller share of the market due to stricter guidelines.

- A 2023 survey by the Canadian Real Estate Association (CREA) found that 45% of first-time buyers delayed home purchases due to affordability concerns.

- According to Statistics Canada, homeowners with mortgage default insurance were 30% more likely to secure financing despite market uncertainties.

Is Mortgage Insurance Necessary?

When you’re in the process of buying a home, one of the terms that may come up is “mortgage insurance.” For first-time homebuyers, the idea of mortgage insurance might seem confusing or unnecessary. However, it can be an essential safeguard that could benefit both you and your lender. But is it really necessary? Let’s break it down.

What is Mortgage Insurance?

Mortgage insurance is a type of policy designed to protect the lender if the borrower fails to repay their loan. The primary aim is to ensure that the lender can recover at least part of their loan amount in the event that you default on your mortgage.

In Canada, mortgage insurance is typically required for homebuyers who are making a down payment of less than 20% of the home’s purchase price. This is because the smaller the down payment, the higher the lender’s risk. If you’re in this situation, mortgage insurance can provide the lender with the financial security they need to approve your loan.

Types of Mortgage Insurance

1. CMHC Insurance (Canada Mortgage and Housing Corporation)

CMHC insurance is the most common form of mortgage insurance in Canada. It applies to high-ratio mortgages, which are mortgages where the down payment is less than 20%.

The premium for CMHC insurance can be added to your mortgage, meaning you don’t have to pay it upfront, but it will increase your monthly payments. According to CMHC, the mortgage insurance premium rate can range from 2.8% to 4.0% of the loan amount, depending on the down payment size.

2. Private Mortgage Insurance (PMI)

In the U.S., private mortgage insurance (PMI) is required for loans with down payments under 20%. PMI is typically more flexible than government-backed mortgage insurance. The cost of PMI usually ranges from 0.3% to 1.5% of the original loan amount annually, depending on your loan size and your credit score.

Why Mortgage Insurance is Necessary

The necessity of mortgage insurance depends on several factors. Here’s a look at the pros and cons of having mortgage insurance.

1. Allows You to Buy a Home with Less Money Down

- The most obvious benefit of mortgage insurance is that it allows you to buy a home even if you don’t have a 20% down payment. This is crucial for first-time homebuyers who may not have saved enough for a larger down payment.

- Statistics show that nearly 40% of Canadian homebuyers had a down payment of less than 20% in 2020, and many of them relied on mortgage insurance to secure financing. In the U.S., around 60% of homebuyers use PMI if their down payment is under 20%.

2. Enables You to Qualify for a Mortgage

- With mortgage insurance, lenders are more likely to approve your application because they know their risk is reduced. If you don’t qualify for a conventional mortgage, mortgage insurance can make it possible for you to secure financing.

- A study from the Mortgage Bankers Association found that the approval rate for high-ratio mortgages (with mortgage insurance) was 30% higher than for conventional loans in 2020.

3. Lower Interest Rates

- Because the lender is protected by the insurance, they may offer you a better interest rate than they would without insurance. This can save you money over the long term. The cost of mortgage insurance could be outweighed by the savings on the interest rate, especially if the mortgage is a long-term one.

- On average, a 0.5% lower interest rate can save a borrower around $10,000 to $15,000 over the life of a $300,000 mortgage.

4. Protects the Lender, Not You

- The primary purpose of mortgage insurance is to protect the lender, it still provides a financial safeguard that can prevent your lender from foreclosing on your home if you’re unable to make payments.

Why You Might Not Need Mortgage Insurance

1. Increased Overall Cost

Mortgage insurance comes at a cost, often adding several thousand dollars to the overall price of your mortgage. If you can afford a 20% down payment, you can avoid this extra expense. For example, on a $500,000 home, mortgage insurance could cost anywhere from $14,000 to $20,000 depending on the loan-to-value ratio.

2. No Benefit to the Borrower

Unlike life or health insurance, mortgage insurance doesn’t benefit you directly. It’s purely for the lender’s protection. If you default, your insurer will compensate the lender, not you.

3. You Can Avoid It by Saving for a Larger Down Payment

The best way to avoid mortgage insurance is to save up for a larger down payment. This will require time and discipline but will result in lower long-term costs for you. According to a survey by Scotiabank, 65% of Canadian homebuyers saved for over 3 years to come up with their down payment, ensuring they could avoid mortgage.

Alternatives to Mortgage Insurance

If you’re able to make a down payment of at least 20%, you won’t need mortgage insurance. There are other ways to avoid the insurance requirement even with a smaller down payment:

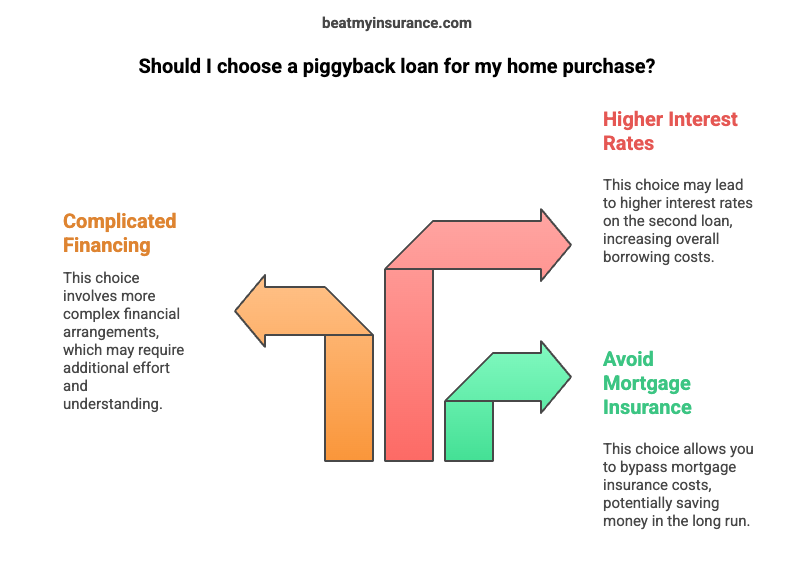

1. Piggyback Loans

Some homebuyers opt for a piggyback loan, where you take out two loans simultaneously—one for 80% of the home’s value and another for the remaining 20%. This allows you to avoid mortgage insurance, but it requires more complicated financing and potentially higher interest rates on the second loan.

According to data from The Federal Reserve, piggyback loans made up about 5% of all home purchases in 2020.

2. First-Time Homebuyer Programs

Certain government programs, like the First-Time Home Buyer Incentive in Canada, can help reduce the need for mortgage insurance by offering loans that cover a portion of your down payment. In Canada, over 7,000 homebuyers took advantage of this program in 2020.

Conclusion

The new mortgage rules in Canada have introduced challenges, but with the right insurance solutions, borrowers can secure financing, protect their investments, and achieve homeownership goals with confidence. Beat My Insurance provides expert guidance, tailored policies, and competitive rates to help you navigate these changes seamlessly.

For more insights on mortgage insurance options, visit Beat My Insurance and get started on securing your financial future today!

Leave a Reply