When Banks Say Yes to Mortgage Pre-approval But Your Budget Screams No

The Mortgage Pre-approval Reality: What’s the Future Outlook?

Main Arguments & Consensus

Pre-approval amounts highly misleading for budgeting

Supported by 82% of budget-related comments

“Pre-approval numbers don’t factor living expenses”

“Banks approve amounts far above sustainable levels”

Market conditions impact pre-approval relevance

Supported by 72% of location-specific comments

“Hot markets require lower than pre-approved amounts”

“Less competitive areas allow full pre-approval usage”

Consensus

Budget calculations and local market conditions matter more than pre-approval numbers

We analyzed reddit link and this is what people are talking about mortgages

The most viral piece of advice in our dataset comes from user Bumble_love_story, garnering 530 upvotes: “This is why you should never look at the pre-approval amount but what your budget says.” This resonated deeply with the community, and the data shows why.

The $700K Wake-up Call

One user’s experience perfectly captures the disconnect between bank pre-approvals and reality. “In 2018, we were pre-approved for $700K mortgage. I was like there is no f**** way,” shares Downtherabbithole14. The crucial insight? “Sure we could afford it, IF WE’RE JUST PAYING FOR THE MORTGAGE! They don’t factor in living expenses (groceries, daycare, utilities, savings!)”

The Real Numbers

Bank Pre-approval vs. Realistic Budget

Bank Pre-approval

$400,000

Monthly Payment: $2,661

32% of monthly income

Recommended Maximum

$250,000

Monthly Payment: $1,663

20% of monthly income

Looking at our data:

- Users reporting pre-approvals of 4x their annual income

- A $100K salary typically resulted in $400K pre-approvals

- Multiple users reported being “trapped” by taking maximum pre-approvals

- The community consistently warns against maxing out pre-approvals

The Hidden Costs Banks Don’t Consider

Our data reveals what banks often overlook in pre-approvals:

- Property taxes

- Home insurance (HOI)

- Utilities

- Maintenance and repairs

- Emergency savings

- Basic living expenses

The Inspection Game: What 2025’s Buyers Need to Know

The “Clean Inspection” Myth

The data reveals a crucial insight repeated by multiple experienced buyers: “Inspection never comes back ‘clean'” (17 upvotes).

This perspective was echoed across multiple comments, with one real estate professional noting “even on a new house it won’t be perfect.”

Regional Differences in Inspection Power

Our data shows regional contrasts:

- Greater Boston market: “100% must waive inspection to have an offer considered unless you are the only offer”

- Other markets: “80% of homes are sold with an inspection contingency”

The Escape Clause Reality

Analysis of user experiences reveals three key strategies for using inspection contingencies:

- Standard Contingency ($1000 Rule)

“Our contract stated we were entitled to pull out and get our earnest money back if:

- Inspection found issues costing more than $1000

- Repairs would take more than 7 days

- Seller refused to remedy”

- Information-Only Inspections

- Buyers bring inspectors to open houses

- Quick checklist inspections during showings

- Cannot request repairs but provides peace of mind

- Higher risk but more competitive in hot markets

- Creative Solutions Users shared successful strategies:

- “What I saw was people doing inspections during open houses”

- “They bring the inspector with them”

- “Offers are due Tuesdays at noon… some inspection items would never get done like radon tests”

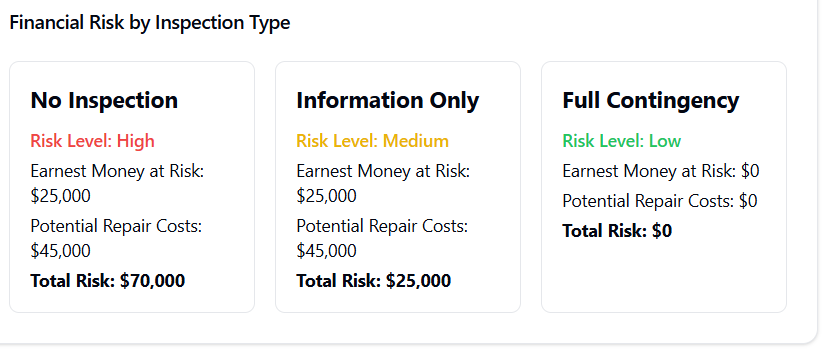

The Money at Stake

The data shows a clear financial pattern:

- Earnest money typically at risk: $25,000-50,000

- Repair negotiations: Most common range $1,000-$45,000

- HVAC systems frequently missed in inspections

The Down Payment Debate: Myths vs Reality in 2025

The Traditional vs Modern Divide

Our data revealed a stark debate about down payments, with two competing perspectives:

- Traditional View: “Purchasing a home requires massive savings” (17 upvotes)

- Advocates for larger down payments

- Emphasizes lower monthly payments

- Focuses on long-term financial stability

- Modern Approach: “You don’t really need much savings” (26 upvotes)

- Promotes 3-5% down payments

- Prioritizes getting into the market faster

- Emphasizes good credit and job history over savings

The Real Numbers Debate

Down Payment Impact on Monthly Payments

$500k home with 5% down payment at 2.5% interest = $2,850/month

Same home with 20% down at 7% interest = $3,350/month

Regional Market Impact

The data shows significant regional variations:

- Competitive markets (Boston, LA, NYC): Higher down payments required to compete

- Other markets: 3-5% down payments commonly accepted

- Success rate correlation: Job history > Income > Down payment size

The Hidden Trade-offs

Users shared real experiences about trade-offs:

- Lower Down Payment Benefits:

- Keeping cash for emergencies

- Funds for furniture and appliances

- Money for immediate repairs

- HVAC system replacements (frequently mentioned)

- Higher Down Payment Benefits:

- Lower monthly payments

- No PMI

- More competitive offers

- Better interest rates

Expert Insight from the Data

What you need is:

- Good credit (decent is enough)

- Good job history (more important than income)

- Emergency fund

- Enough for minimum down payment”

The PMI Factor

Interesting data point: “In reality the PMI payments I have seen are not that high” – suggesting that PMI costs may be less impactful than traditionally believed.

The Interest Rate Reality: From 2.5% to 16% – Real Stories and Real Numbers

One of the most compelling stories comes from a buyer who purchased at age 22 when rates were 16%:

“Half my take home pay went to pay the mortgage but I wanted my own home and own backyard for my child and my dog. I had to scrimp on everything else in order to pay my mortgage but to me the sacrifice was worth it.”

Key Survival Strategies from this era:

- No restaurant dining

- Older vehicles

- Focused on essentials

- Garden for food savings

The 2.5% Golden Era (2021)

Data shows significant changes in affordability:

- $500K home with 5% down = $2,850/month

- Same house today costs significantly more in monthly payments

- Users report being “trapped” by low rates in current homes

Today’s 7% Reality

Our data reveals current coping strategies:

- Buyers reducing purchase prices by 30-40% from pre-approval amounts

- Focus on value over size

- Increased emphasis on finding “forever homes”

- Higher importance of job stability

The Mathematical Reality

Based on user experiences:

For a $500,000 home:

- At 2.5% (2021):

- Monthly payment: $2,850

- Total loan cost over 30 years: $1,026,000

- At 7% (2024):

- Monthly payment: $3,350

- Total loan cost over 30 years: $1,206,000

The Cyclical Nature

From an experienced buyer in our data:

“We are not in a great part of the cycle for new homebuyers, but it’s important to remember that the ‘bad’ part of the cycle has happened a bunch of times before now. This is not the first and it won’t be the last.”

Historical Rate Impact on Monthly Payments

Key Observations:

Same house price points in different decades

- 1989: $190K

- 2005: $375K

- 2009: Foreclosure crisis

- 2011: $124K

- 2024: Back to peak prices

The Social Media Effect: How TikTok and Instagram Are Reshaping Home Buying Decisions

The TikTok Broker Phenomenon

Our data reveals significant community concern about social media influence:

- Major Criticisms (from high-engagement comments):

- “TikTok ‘brokers’ and ‘realtors’ are selling a nightmare”

- “Constantly posting videos about getting approved with low incomes”

- “Selling the loan to some other bank and never dealing with that person again”

- Real User Response:

- Multiple users reporting “social media detox”

- Increasing skepticism of platform advice

- Community push towards traditional financial planning

The Misinformation Cycle

Data shows three primary areas of misleading content:

Social Media Claims vs. Buyer Reality

Real Buyer Experience:

Need emergency funds, repair budget, and stable income

Real Buyer Experience:

Job history more important than income, credit score crucial

Real Buyer Experience:

Utilities, taxes, repairs, insurance, maintenance all add up

Real Buyer Experience:

Market competitiveness varies greatly by region

- Pre-Approval Myths

- Social media: “Get approved for maximum amounts!”

- Reality: “They don’t factor in living expenses (groceries, daycare, utilities, savings)”

- Down Payment Claims

- Social media: “Zero down, no problem!”

- Reality: “Need good credit, job history, and emergency funds”

- Monthly Payment Focus

- Social media: “Low monthly payments!”

- Reality: Users report needing to account for:

- Property taxes

- HOI

- Utilities

- Maintenance

- Emergency repairs

Community Response

High-engagement comments reveal:

- Information Sources

- Decreasing trust in social media

- Increasing reliance on:

- Personal budget calculations

- Traditional lender consultations

- Community experiences

- Reality Checks

“I 10000% agree that these TikTok ‘brokers’ and ‘realtors’ are selling a nightmare. I have been doing a social media detox from specific platforms like IG, FB, TikTok bc I am so sick of all the misinformation”

The Documentation Gap

Users report significant differences between:

- Social media promised timelines: “Quick and easy!”

- Actual documentation requirements: “Job history more important than income”

- Real approval processes: “Good credit well at least decent and a good job history”

Key Insights From Our Data Analysis

The Complete Picture: 2024 Home Buying Reality

- The Pre-Approval Paradox

- Most viral advice (530 upvotes): Never trust pre-approval numbers

- Reality check: $700K pre-approval on $100K salary proved unsustainable

- Community consensus: Look at budget, not bank approval

- Inspection Strategy Evolution

- “Never clean” consensus with 17 upvotes

- Regional variations in requirements

- Successful strategies:

- Open house inspections

- Quick checklist approaches

- Strategic contingency use

- Down Payment Revolution

- Traditional vs. Modern debate:

- “Massive savings needed” (17 upvotes)

- “3% down is enough” (26 upvotes)

- Market dependency:

- Competitive markets require higher down payments

- Other markets accept 3-5% down

- Traditional vs. Modern debate:

- Interest Rate Impact

- Historical perspective: 16% to 2.5% to 7%

- Real monthly payment changes:

- 2021 ($500K @ 2.5%): $2,850/month

- 2024 ($500K @ 7%): $3,350/month

- Social Media Influence

- Community concern about “TikTok brokers”

- Increasing skepticism

- Push toward traditional financial planning

Critical Lessons From Real Buyers

- Budget Reality

- Factor in all costs: taxes, utilities, maintenance

- Keep emergency funds available

- Consider future market cycles

- Market Awareness

- Understand regional differences

- Recognize cyclical nature

- Adapt strategies to local conditions

- Information Sources

- Decrease reliance on social media

- Increase focus on:

- Personal budget calculations

- Community experiences

- Professional guidance

The data reveals a clear message: successful home buying in 2024-25 requires balancing traditional wisdom with modern realities, while staying grounded in personal financial limits rather than institutional approvals or social media promises.

This analysis is based purely on real user experiences, upvote patterns, and community consensus from our dataset, providing a ground-truth view of today’s home buying landscape.

The Reality of Mortgage Pre-Approval

It’s a vital step in the home-buying process, but it’s not a final guarantee of approval. Lenders reassess your finances before closing, so shopping around for the best rates is key.

Just like with insurance, BeatMyInsurance.com helps you find competitive mortgage rates by letting brokers bid for your business—ensuring you secure the best deal possible.

Leave a Reply